Foreign Account Tax Compliance Act

(FATCA): Entity Classification Guide

October 2015

Contents

Introduction ................................................................................................................................................ 1

1. Which W-series form should I complete for the entity? ............................................................................ 3

1.1. Does the entity need to provide a Form W-9? ........................................................................................ 4

1.2. Is the entity acting as a beneficial owner or an intermediary?................................................................... 4

1.3. Does the entity need to provide a Chapter 3 Status on the W-form? ......................................................... 5

2. Classification Overview ....................................................................................................................... 6

2.1. Which Inter Governmental Agreement (IGA) does the entity fall under and why does it matter? ................... 6

2.2. FATCA Entity Classification Process Overview ...................................................................................... 7

3. Is the entity a Financial Institution? ....................................................................................................... 9

3.1. Completion of W-8 series form as a Financial Institution (FI) ................................................................... 9

3.2. How to determine if the entity is a Financial Institution (FI)?..................................................................... 9

3.3. If the entity is a Financial Institution (FI), what next? ............................................................................. 11

3.4. If the entity is not a Financial Institution (FI) what next? ........................................................................ 12

4. FIs in IGA jurisdictions: Is the entity a type of Non Reporting IGA Financial Institution (FI)? ....................... 13

4.1. Is the entity an Exempt Beneficial Owner? .......................................................................................... 13

4.2. Is the entity a Deemed Compliant Investment Entity? ........................................................................... 14

4.3. Is the entity a Registered / Certified Deemed Compliant Entity? ............................................................. 15

5. FIs in non IGA jurisdictions: Is the entity a type of US Treasury Regulations Non Reporting Financial

Institution (FI)? ................................................................................................................................ 16

5.1. Is the entity an Exempt Beneficial Owner? .......................................................................................... 16

5.2. Is the entity a Deemed/ Certified Deemed Compliant Investment Entity?................................................. 17

5.3. Is the entity a Registered or Certified Deemed Compliant Entity? ........................................................... 18

6. Is the entity a Non Financial Foreign Entity (NFFE)? ............................................................................ 19

6.1. NFFEs other than Passive NFFEs ...................................................................................................... 20

6.2. Passive NFFEs ................................................................................................................................ 21

7. Glossary ......................................................................................................................................... 22

1

Introduction

What is FATCA?

The US Treasury has enacted a piece of legislation known as the Foreign Account Tax Compliance Act (“FATCA”)

which aims to detect and deter US Persons from using non-US financial organisations to evade US tax. It requires

Financial Institutions (FIs) such as HSBC Global Private Bank (GPB) to identify customers that are US Persons and

accounts owned either directly or indirectly by US Persons. Further, many countries have signed ‘Intergovernmental

Agreements’ (“IGAs” or “Agreements”) with the US to agree to implement this legislation domestically.

For HSBC Global Private Bank (GPB) (“us/we”) to comply with this legislation, we require you to complete the

appropriate IRS (Internal Revenue Service) W-series form confirming the entity’s FATCA classification (also known

as Chapter 4 status). It is the information on this form (and supporting documentation where appropriate) that we

will rely upon to fulfil our legislative reporting requirements where necessary in respect of FATCA and US Persons.

Why have I received this document?

The entity classification rules under FATCA are complex and determining the entity’s FATCA classification is not a

straight forward process. Further, some entities will find that they have multiple classifications available to them and

will need to consider which classification is the most appropriate for them. We are not able to provide tax advice or

advise customers on their FATCA classification.

This document is not intended to answer all questions or cover all scenarios but should give you an introduction to

the FATCA entity classifications and a summary of the key determining factors, using visual decision trees to

summarise these. Detailed classification definitions are outlined in the glossary to this document.

If you do not wish to use this document we would strongly recommend you seek appropriate tax advice to assist

you with the classification process.

The steps required are as follows:

Step A

Which W-series form should I use?

You must document the entity’s FATCA classification on the appropriate W-series form. The flow chart

in Section 1 outlines the considerations necessary to determine which W-series form to complete.

Section 2 then provides links to the various W-series forms and guidance on how to complete them.

Step B

Determine the applicable entity classification rules

The classification rules differ depending on the entity’s jurisdiction of tax residence. Section 3 outlines

the relevant local rules that you will need to take into consideration when determining the entity’s

classification.

Step C

Determine the entity’s FATCA classification

With reference to the appropriate legislation, you should then determine the FATCA classification by

considering the nature and activities of the entity. In some cases, there will be multiple options

available. In these situations, we recommend you seek appropriate tax advice.

The high level classification process is outlined in Section 3, followed by the definition of Financial

Institutions in Section 4. The remaining sections then detail the Financial Institution classifications in

Sections 5 and 6 and the Non Financial Foreign Entity classifications in Section 7.

Case studies and examples of Financial Institutions and Non Financial Foreign Entities are provided on

pages 10 and 21 respectively.

Some entity classifications will require you to provide additional documentation to us.

These classifications have been highlighted with the following symbol:

In these cases, the additional documentation requirements are clearly detailed.

2

What if I still don’t know what the entity’s FATCA classification is?

If you get to the end of this document and are still unclear how to establish the entity’s FATCA classification or are

uncertain of its classification, you will need to seek appropriate tax advice. Your Relationship Manager at HSBC

Global Private Bank will not be in a position to provide assistance beyond the information contained within this

guide given the complexity of the entity classification rules and given that by law the Bank is not permitted to give

tax advice.

This document is not intended and cannot be used as a substitute for a detailed analysis of the Foreign Account

Tax Compliance Act (FATCA), Intergovernmental Agreements or related documents. This document does not

constitute or should not be construed as tax advice. In case of uncertainty, please obtain professional tax advice.

This document is intended to assist you in identifying and completing the documentation necessary for FATCA

classification purposes, based on FATCA information currently available.

This document contains visualizations of the "decision tree" in a simplified form. To accurately determine the

FATCA please refer to the textual description.

We recommend that entities seek professional tax advice in the case of uncertainty or if there are several

classifications that may be applicable to the entity.

3

1. Which W-series form should I complete for the entity?

We require you to complete an IRS W-series form confirming the entity’s FATCA classification. There are a suite of

W-series forms and you will need to establish which is the correct form to provide us with. To do so, you must

consider the entity’s US/non-US status and whether it is the beneficial owner or an intermediary in respect of the

account in question.

Please consult the below flow diagram and the indicated sections within this guidance document to help determine

which W-series form you should complete. Further guidance on which form to complete can be found on the W-

series forms themselves and in the IRS instructions to these as set out below.

Please see the below links to the W-series forms and accompanying IRS instructions. Further information, including

FAQs, is also available on the FATCA section of our website at: http://fatca.hsbc.com/en/gpb

Non-US intermediaries and flow-through entities that are

Non-US entities and certain US branches.

These entities will also need to provide the relevant W-series

form(s) for the beneficiaries. See Section 1.2.

US Entity

Non-US government, international organisation, Non-US

central bank of issue, Non-US tax-exempt organisation or

foreign private foundation

Beneficial owners that are non-US entities

Non-US person claiming that income is effectively connected

with the conduct of a trade or business in the United States

Step A

W-9 Form: http://www.irs.gov/pub/irs-pdf/fw9.pdf

W-9 Form Guidance: http://www.irs.gov/pub/irs-pdf/iw9.pdf

W-8BEN-E Form: http://www.irs.gov/pub/irs-pdf/fw8bene.pdf

W-8BEN-E Form Guidance: http://www.irs.gov/pub/irs-pdf/iw8bene.pdf

W-8BEN Form: http://www.irs.gov/pub/irs-pdf/fw8ben.pdf

W-8BEN Form Guidance: http://www.irs.gov/pub/irs-pdf/iw8ben.pdf

W-8IMY Form: http://www.irs.gov/pub/irs-pdf/fw8imy.pdf

W-8IMY Form Guidance: http://www.irs.gov/pub/irs-pdf/iw8imy.pdf

W-8EXP Form: http://www.irs.gov/pub/irs-pdf/fw8exp.pdf

W-8EXP Form Guidance: http://www.irs.gov/pub/irs-pdf/iw8exp.pdf

W-8ECI Form: http://www.irs.gov/pub/irs-pdf/fw8eci.pdf

W-8ECI Form Guidance: http://www.irs.gov/pub/irs-pdf/iw8eci.pdf

See

Section 1.1

See

Section 1.2

US

Entity?

Beneficial

Owner?

W-9

W-8EXP

W-8BEN-E

W-8ECI

W-8IMY

No

Yes

Yes

No

4

1.1. Does the entity need to provide a Form W-9?

US entities should complete a Form W-9. Should the entity be a US entity, there is no further need to consult this

guide as the remainder of the guide deals with the classification of non-US entities.

Broadly a US entity is any of the following:

A Corporation or Partnership created or organised in the US or under the law of the US or of any state in the

US.

An estate of a US person or a trust if a court within the United States is able to exercise primary supervision

over the administration of the trust and one or more US persons have the authority to control all substantial

decisions of the trust.

The US government or any agency/instrumentality thereof.

You should obtain tax advice if you are unsure whether the entity is considered a US entity.

Please also note that a Form W-9 and, outside the US, a secrecy waiver from the substantial US owner (in

addition to a Form W-8BEN-E from the entity) may be required if you conclude that the entity is a Passive

NFFE AND it has ‘substantial US owners’ (defined below).

Substantial US owners

In general, substantial US owners in the case of corporations are any persons that own directly or indirectly more

than 10% of the stock of such corporation and in the case of a trust, any person treated as an owner of any portion

of a trust treated as a grantor trust under US tax law and any person that holds directly or indirectly more than 10%

of the beneficial interests of the trust AND that are specified US persons. Generally a “specified US person” is any

US person other than those specifically excluded, such as a publicly-traded corporation and affiliates thereof, a tax-

exempt organisation, a US or state governmental entity, a bank, a broker, a dealer, a regulated investment

company, a real estate investment trust, a common trust fund, a charitable trust and certain tax-exempt trusts.

A US person in respect of an individual is commonly a citizen or resident of the United States and they can be

treated as a US person even if they reside permanently outside the US or even if they hold a non-US passport.

The Bank may already have the appropriate documentation on file in respect of the entity’s US owners. Therefore if

you conclude that the entity is a Passive NFFE or Owner Documented FFI (“ODFFI”) and there are US persons

amongst the entity’s owners we recommend you contact your Relationship Manager to confirm what documentation

is already held on file in respect of those US persons. Generally a Passive NFFE must provide a list of its

substantial US owners on the Form W-8BEN-E or on a withholding statement provided with a Form W-8IMY. An

ODFFI must provide W-series tax forms for all its underlying beneficial owners. Curative documentation is required

for all non-US owners with US indicia (including W-series forms in the case of a Passive NFFE with non-US owners

that have US indicia).

1.2. Is the entity acting as a beneficial owner or an intermediary?

Determining who the beneficial owner of an account is can be complex. Generally, an account holder is the

beneficial owner of that account if they own the assets or income within the account or they are entitled to them.

An account holder is acting as an intermediary if they receive amounts from the account on behalf of another

person or as a “flow-through entity”. Common examples include qualified intermediaries (QIs), nonqualified

intermediaries (NQIs), non-US simple trusts, non-US grantor trusts, and non-US partnerships. Where the entity is

acting as an intermediary, we will require you to provide the Form W-8IMY (unless you consider another form more

appropriate) and with this, a withholding statement containing pooled information for QIs or, in the case of

nonqualified intermediaries and non-withholding non-US partnerships and trusts the details of the beneficial owners

and income allocation percentages and, the appropriate W-series form(s) for those beneficial owners.

The determination of US trust type is a complex process. The box below provides common examples where the

settlor is a non-US person and the trust is not marketing itself to third parties (i.e., it is a trust established for the

benefit of family members, relatives or charities).Tax advice should be sought if you are unsure of the trust

type under US tax law.

5

1.3. Does the entity need to provide a Chapter 3 Status on the W-form?

This document focuses on the types of FATCA entity classification and how to determine these for the entity.

However when completing the applicable W-series form, entities must also document their Chapter 3 status. The

Chapter 3 determination requires you to classify the entity as one of the following depending on whether the entity is

completing a Form W-8BEN-E or a Form W-8IMY:

W-8BEN-E

W-8IMY

Corporation

Qualified Intermediary

Partnership

Non-Qualified Intermediary

Complex Trust

Territory Financial Institution

Grantor Trust

US branch

Simple Trust

Withholding foreign partnership

Private Foundation

Withholding foreign trust

Central bank of Issue

Nonwithholding foreign partnership

Tax-exempt organisation

Nonwithholding foreign simple trust

Estate

Nonwithholding foreign grantor trust

Government

Disregarded entity

Similarly, the “Type of Entity” line should be completed on Form W-8EXP and Form W-8ECI.

In particular, if the entity is a trust, the determination of trust type under US tax law (e.g., foundations assimilated to

trusts) can be complex. Whilst we have provided common examples for trusts in Section 1.2, you should consider

seeking appropriate tax advice if you are unsure as to the entity’s Chapter 3 status.

Entities set up as a corporation, e.g., a PIC, would generally tick the “Corporation” check box, LLCs should tick

“Corporation”, “Partnership” or “Disregarded entity” as applicable.

Once you have determined which W-series form must be completed, please proceed to Section 2 on the

next page in order to determine the entity’s FATCA classification.

Non-US Grantor trust: Trusts where the settlor of the trust can revoke the trust or the settlor and/or their spouse

are the only ones entitled to income whilst alive. In that case, the grantors are considered to be the beneficial

owners.

Non-US Simple trust: Trusts where all income in the year must be distributed. No income can be accumulated for

charitable purposes and no distributions in excess of income can be made for the year. The beneficiaries of the

trust are considered to be the beneficial owners.

Non-US Complex trust: Trusts that are not deemed to be simple or grantor trusts (generally irrevocable and

discretionary trusts). The trust itself is considered to be the beneficial owner and would provide a Form W-8BEN-E.

6

2. Classification Overview

2.1. Which Inter Governmental Agreement (IGA) does the entity fall under and

why does it matter?

Although FATCA is a piece of US legislation, a number of governments have entered into IGAs with the US and

have effectively implemented FATCA into domestic law.

As such, there are variances across the IGAs and domestic law in the types of FATCA classification. Given this, you

will need to consider if the entity’s country of tax residence has signed an IGA as this information will be necessary

to understand the entity’s FATCA classification. A full list of the IGAs that have been signed is available on the IRS

website (http://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA-Archive.aspx).

Tax authorities in each jurisdiction are also in the process of issuing country specific guidance notes in respect of

FATCA. . Therefore, you should consult the IGA of the entity’s tax residence, together with any locally issued

guidance from the tax authorities, to determine the entity’s final FATCA classification.

Entities that are tax resident in jurisdictions with no IGA in place should refer to the US Treasury Regulations which

can be found on the IRS FATCA website:

http://www.irs.gov/Businesses/Corporations/Foreign-Account-Tax-Compliance-Act-FATCA

This document does not provide guidance on tax residence. If you are unsure of the entity’s tax residence

you should seek tax advice.

Step B

7

2.2. FATCA Entity Classification Process Overview

The flow chart below summarises the key considerations that you should take to help reach the classification

options available to the entity. You should consult this document where referenced below for assistance in

determining the entity’s classification.

Start

(with reference to the

entity’s tax residence

and applicable

classification rules as

identified in section 3.1):

Is the entity a

Financial Institution?

Is the entity tax

resident in a

jurisdiction that has

signed an IGA?

Does the entity meet

any of the Exempt

Beneficial Owner

classifications?

Does the entity meet

any of the Deemed

Compliant Investment

Entity classifications?

Does the entity meet

any of the other

Registered/Certified

Deemed Compliant

classifications?

Registered Deemed

Compliant

Local Client Base

Non reporting members

of participating FFI group

Restricted Fund

Qualified Credit Card

Issuers and Servicers

Certified Deemed Compliant

Local Bank

FFIs with only low-value

accounts

Limited life Debt

Investment Entity

Investment advisors and

managers

Registered Deemed Compliant

Local FFI

Non reporting members of

participating FFI group

Restricted Fund

Qualified Credit Card

Issuers and Servicers

Certified Deemed Compliant

Local Bank

FFIs with only low-value

accounts

Limited life Debt Investment

Entity

Investment advisors and

managers

Restricted Distributor

Territory FI

Reporting Model 1 or 2 FFI

Deemed Compliant

Investment Entities

Trustee documented trust

(IGA only)

Sponsored Investment

Entity

Sponsored Closely Held

Investment Vehicle

Owner Documented FFI

Collective Investment

Vehicles

Exempt Beneficial Owners

Governmental

organisation

International Organisation

Central Bank

Retirement Plan

Entity wholly owned by

EBOs

NFFEs other than Passive NFFEs

Publicly Traded or affiliate thereof

Active NFFE: <50% Passive Income

Entity in liquidation/bankruptcy

Excepted Territory NFFE

Excepted Inter-affiliate FFI

Start-up company

Nonfinancial group entity

Non-profit or 501(c) organisation

Passive NFFE

Passive

Sponsored Direct Reporting

Direct Reporting

See

Section 3.2

for guidance

See Section

2.1 for

guidance

See

Section 4.1

for guidance

See

Section 4.2

for guidance

See

Section 4.3

for guidance

See

Section 5.1

for guidance

See

Section 5.2

for guidance

See

Section 5.3

for guidance

See

Section 6 for

guidance

No

No

Yes

Yes

No

Yes

No

No

Yes

Yes

Yes

No

Yes

Yes

No

Yes

No

No

Participating FFI

Does the entity

meet any of the

NFFE

classifications

other than

Passive?

Does the entity meet

any of the Exempt

Beneficial Owner

descriptions?

Does the entity meet

any of the Deemed

Compliant Investment

Entity classifications?

Does the entity meet

any of the other

Registered/Certified

Deemed Compliant

classifications?

8

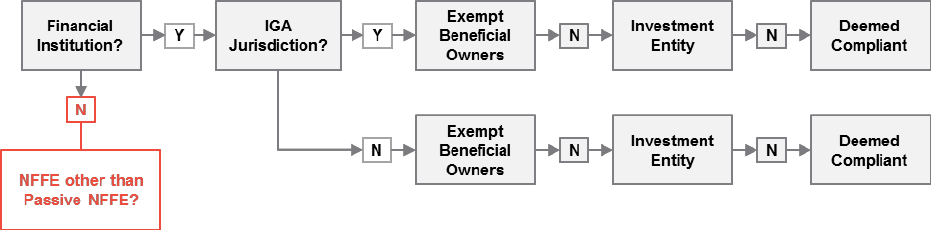

A non-US entity that is not classified as one of the above classifications will be considered a Nonparticipating FFI.

Document Reference

The above classification overview, in the below simplified format, is positioned at the start of each

subsequent section. The red outline identifies the part of the classification process under consideration.

9

3. Is the entity a Financial Institution?

3.1. Completion of W-8 series form as a Financial Institution (FI)

If the entity has already undertaken an exercise to determine its status as a FI, you should complete the applicable

W-8 series form as a Reporting Model 1 FFI, Reporting Model 2 FFI or Participating FFI (unless a Non-

Reporting IGA FFI), as determined by the entity’s jurisdiction of tax residence. Please complete the relevant W-

series form as identified in Section 1 and include the entity’s Global Intermediary Identification Number (GIIN)

(generally in box 9 of the W-series Form).

If you are unsure of the entity’s FATCA classification, please proceed through this section for further guidance.

3.2. How to determine if the entity is a Financial Institution (FI)?

Broadly, there are five types of FI definition as set out below. You will need to consider all the FI definitions to

establish whether the entity is a FI. It may be possible for the entity to meet more than one definition of FI.

Please consider ALL of the descriptions and examples below and consider if the entity falls into any of the

categories. If the entity falls within one or more of these categories, it will be a FI. If the entity does not fall within

any of these categories and you are comfortable that there are no local variances that would mean otherwise, the

entity will be a Non Financial Foreign Entity (NFFE).

We note that you may see references in this document to a ‘FFI’, this stands for Foreign Financial Institution and is

the terminology used in the US regulations. Broadly the definition of a FI is aligned across US legislation and local

country’s legislation but we would recommend that you refer to the entity’s local legislation or seek independent tax

advice to verify if the entity is a FI as the exact definitions may vary depending on which jurisdiction the entity is tax

resident in.

Further, FIs may be required to register with the IRS and may have the responsibility to carry out a number

of additional obligations under domestic or US law. Therefore if you consider that the entity is a FI we

recommend you seek tax advice to understand the entity’s obligations further.

Step C

10

3.2.1. Investment Entity

Consideration

Does the entity conduct any of the following activities

for or on behalf of a customer:

Trading in money market instruments;

Individual and collective portfolio management; or

Otherwise investing, administering, or managing

funds or money on behalf of other persons

Does this consist of a significant portion of the entity’s

business (more than 50%)?

Or

Is the entity’s income primary attributable (more than

50%) to investing, reinvesting or trading in financial

assets and the entity is managed by a Financial

Institution?

Or

Is the entity or its activities professionally managed?

Examples

Trusts with a professional trustee;

Fund managers;

Professionally managed personal investment

companies;

Funds with a fund manager

Note: The above is guidance only. There are different definitions for an "investment entity" under the Treasury

Regulations and IGAs. Under the Treasury Regulations, a two-part test must be satisfied: (i) an income test; and (ii)

the entity must be managed by a "professional manager". Under the IGA definition, only professional management

is required to meet the investment entity definition unless the local IGA allows the US Treasury Regulations to be

applied in lieu of corresponding definitions in the Agreement. Further guidance is expected from the IRS in this

regard and it is therefore recommended that you seek tax advice if you believe the entity may meet any of these

conditions.

Case Study: Trusts

Trusts may fall under the definition of Investment Entity where the trust is professionally managed. A trust will be

professionally managed where ANY of the below are true:

The trustee is a

Financial Institution.

The trustee (on behalf of the trust)

engages a Financial Institution to

manage the trust.

The trustee (on behalf of the trust) engages a

Financial Institution to manage the trust’s financial

assets.

A Financial Institution will manage the

trust where it has been appointed by

the trustees to carry out the day to

day functions including management

functions of the trust on behalf of the

trustees.

A Financial Institution manages the financial assets

of the trust where it manages the investment

strategy for the assets.

This will usually be where the trust has appointed a

discretionary fund manager to manage the portfolio.

The holding or acquisition of a retail type product or

service (such as units purchased in investment

funds) will not meet this condition. Likewise, the

holding of a fixed asset (such as insurance products

or investment bonds) will not constitute professional

management of the assets of the trust.

Professionally Managed

Trusts, Personal Investment Companies, LLCs

and Partnerships and Investment Funds may fall

into the investment entity definition for being

professionally managed.

An entity will be professionally managed if it is

managed by a FI. A FI will manage an entity where

it has been appointed to carry out the day to day

functions of that entity.

Entities that have appointed a discretionary fund

manager will generally be considered to be

professionally managed.

The principles in the below trust case study are

relevant to the above entity types. See also related

discussion in Section 6.2.

11

3.2.2. Custodial Institution

Considerations

Does the entity hold financial assets for the account of

others?

Financial assets include securities (such as corporation

stocks, notes, bonds, debentures, partnership interests,

commodities, notional principal contracts, and insurance

or annuity contracts).

Is this a substantial part of its business (more than 20%

of income)?

If yes to the above, the entity is likely to be a custodial

institution.

Examples

• Custodial banks;

• Brokers;

• Trust companies;

• Clearing organisations and nominees;

• Entities carrying out regulated activities, e.g. in the

UK by the FSMA;

• Employment Benefit Trust holding shares for an

employee after they have been granted

3.2.3. Depositary Institution

Considerations

Does the entity accept deposits in the ordinary course of

a banking or similar business?

Examples

Entities carrying out regulated activities, e.g., in the UK

by the FSMA generally are:

• Saving or Commercial Banks;

• Credit Unions;

• Industrial and Provident Societies;

• Building Societies;

• Entities that issue payment cards that can be pre-

loaded with funds in excess of $50,000 to be spent

at a later date

3.2.4. Specified Insurance Company

Considerations

Does the entity carry out insurance activities?

Does it issue Cash Value Insurance or Annuity

Contracts?

Examples

An Insurance company that only provides the following

services would generally not be treated as a FI:

General Insurance;

Term life insurance; or

Reinsurance companies that only provide indemnity

reinsurance contracts.

3.2.5. Holding Companies and Treasury Centres of Financial Groups

Considerations

Is the entity a holding company of one or more entities that are

FIs? Or;

Is the entity a treasury centre whose primary activity includes

entering into hedging and financing transactions with or for FIs?

The treatment of holding companies and

treasury centres varies across jurisdictions.

Please consult your professional tax advisor

to determine the relevant requirements.

Proceed to Section 3.3 if you DO consider that the entity meets one of the above categories of FI. If you do

NOT consider that the entity meets any of these definitions, it is likely to be a Non Financial Foreign Entity

(NFFE) and you should proceed to Section 3.4.

12

3.3. If the entity is a Financial Institution (FI), what next?

If you consider that the entity should be classified as a FI, you should consider seeking tax advice as the entity may

need to register with the IRS as a Reporting Model 1, Reporting Model 2 or Participating Financial Institution and

may have certain FATCA obligations.

FIs that meet certain conditions may not have to register and may not have any due diligence and reporting

obligations under FATCA. To determine if this is the case, you will need to consider if the entity is a Non-Reporting

FI and consider the relevant legislation for the entity’s jurisdiction of tax residence. For a reminder of the

significance of this consideration, please see Section 2.1.

FIs that are tax resident in a jurisdiction with an IGA in place should proceed to Section 4 and refer to the relevant

IGA to determine if they are a Reporting FI or a Non Reporting FI and to confirm their classification. If the entity is a

FI and does not meet any of the Nonreporting FI classifications in Section 4, you should complete the W-series

form as a Reporting FI.

FIs that are tax resident in jurisdictions with no IGA in place should proceed to Section 5 and refer to the US

Treasury Regulations to determine if they are a Reporting FFI or a Non Reporting IGA FFI and to confirm their

classification. If the entity is a FFI and does not meet any of the classifications in Section 5, you should complete

the W-series form as a Reporting Model 1 FFI, Reporting Model 2 FFI, Participating FFI or Nonparticipating FFI.

3.4. If the entity is not a Financial Institution (FI) what next?

If you do not think the entity meets any of the above definitions, proceed to Section 6 to understand the

classifications for non Financial Institutions, known as Non-Financial Foreign Entities (NFFEs). There are a number

of types of NFFE; an NFFE may be classified as a ‘Passive’ NFFE. Passive NFFEs are required to provide

information on the US owners of the entity (known as ‘substantial US owners’). See Section 1.1 for further details.

NFFEs generally will not be required to register with the IRS (unless they are Direct Reporting NFFEs or Sponsored

Direct Reporting NFFEs), but still need to provide us with the appropriate W-form documenting their chapter 4

status for FATCA purposes.

13

4. FIs in IGA jurisdictions: Is the entity a type of Non Reporting IGA

Financial Institution (FI)?

This section summarises the Non-Reporting FI classifications options available for entities that are tax resident in a

country that has signed an IGA (see Section 2). For all Non-Reporting IGA FI classifications, account holders

should complete section XII on the Form W-8BEN-E or section XVIII on the Form W-8IMY (where the entity is an

intermediary or flow through entity). When completing the applicable W-series form (Section 1), entities must state

(in section XII/XVIII) which IGA jurisdiction they are tax resident in and state their FATCA entity classification.

The below guidance should be used with reference to Annex II of the entity’s applicable IGA as there are local

variances and we would recommend obtaining independent tax advice if you think the entity meets one of these

classifications.

4.1. Is the entity an Exempt Beneficial Owner?

Exempt Beneficial Owners (EBOs)

Governmental

Organisation

The entity is a

non US

government or

political

subdivision

thereof

International

Organisation

International or

supranational

organisation

whose income

does not benefit

private persons

Central Bank

An institution that

is the principal

authority in issuing

instruments

intended to

circulate as

currency

Retirement Plan

A fund to provide

retirement benefits

to current or former

employees. Each

IGA lists retirement

funds that qualify

as Exempt

Beneficial Owners

Entity wholly

owned by EBOs

An Investment

Entity where the

equity interest is

wholly owned by

an Exempt

Beneficial Owner

and any debt

interest by an

Exempt Beneficial

Owner or

depository

institution

1

2

3

4

5

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

Additional Documentation Requirements

An Entity wholly owned by EBOs must complete a FFI Owner Reporting Statement which can be found at HSBC’s

FATCA website: http://fatca.hsbc.com. In addition, the legislation requires us to obtain documentation from those

owners. HSBC Global Private Bank policy requires this to be the appropriate W-series form to align with existing

bank policies.

If you believe the entity does NOT meet any of the above descriptions, please proceed to Section 4.2.

14

4.2. Is the entity a Deemed Compliant Investment Entity?

If the entity is an Investment Entity there may be multiple classifications available to it. If you believe the entity does

do not meet any of the below descriptions, please proceed to Section 4.3.

Deemed Compliant Investment Entities

Trustee

Documented

Trust

The trustee as a

Financial

Institution for

FATCA purposes

itself, undertakes

all FATCA

responsibilities

for the trust

Sponsored

Investment

Entity

An Investment

Entity whose

FATCA

responsibilities

are undertaken by

a sponsor

See detail below

Sponsored

Closely Held

Investment

Vehicle

An Investment

Entity with 20 or

fewer owners with

a sponsor

See detail below

Owner

Documented FFI

An entity that

provides to us

details of all

owners and

documentation for

these owners and

therefore does not

require registration

Collective

Investment

Vehicles

Investment Entities

that are regulated

as Collective

Investment

Vehicles where the

interests in the

entity meet certain

requirements.

6

7

8

9

10

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

Additional Documentation Requirements

Owner Documented FFIs must complete a FFI Owner Reporting Statement which can be found at HSBC’s FATCA

website: http://fatca.hsbc.com

In addition, the legislation requires us to obtain documentation from those owners. HSBC Global Private Bank policy

requires this to be the appropriate W-series form to align with existing bank policies.

Sponsored Entities

There are some classification options where the entity agrees with another entity that it will be its sponsor. By

sponsoring the entity, the sponsor agrees to take on a number of FATCA obligations on its behalf and is likely to

need to register with the IRS.

Should you be interested in a sponsoring arrangement we recommend that you discuss this with the potential

sponsor and obtain tax advice.

HSBC would not generally act as a sponsoring entity except where HSBC are responsible for administering the

entity.

15

4.3. Is the entity a Registered / Certified Deemed Compliant Entity?

There are further registered deemed-compliant and certified deemed-compliant entity classifications available:

Registered Deemed Compliant (RDC)

Local Client Base

The entity has a local

client base (at least

98% of its accounts are

held by residents of its

country)

Non reporting member

of participating FFI

groups

A Financial Institution

part of a participating

FFI group that

implements procedures

to close or transfer

reportable accounts to

another FI within the

group

Restricted Fund

Entity with prohibitions

on the sale of units in

the fund to specified US

Persons, NPFIs and

Passive NFFEs with

substantial US owners.

Qualified Credit Card

Issuers and Servicers

The entity is an issuer of

credit cards that accept

deposits only when a

customer makes a

payment in excess of a

balance

11

12

13

14

Certified Deemed Compliant (CDC)

Local Bank

The entity must be

operating solely as a

bank and must not have

a fixed place of

business outside of its

country of incorporation.

FFIs with only low-

value accounts

For FIs that are not

investment entities that

have no accounts with a

value exceeding

$50,000

Limited life debt

investment entity

A securitisation

company created to hold

debt until maturity or

until liquidation of the

vehicle

Investment advisors

and managers

Entity must be in the

business of providing

investment advice

and/or managing

investments for clients.

15

16

17

18

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

16

5. FIs in non IGA jurisdictions: Is the entity a type of US Treasury

Regulations Non Reporting Financial Institution (FI)?

This section summarises the Non-Reporting FI classifications options available under the US Treasury Regulations

(see Section 2) which apply to entities in non IGA jurisdictions. The relevant W-8BEN-E or W-8IMY sections for

entities to complete are listed for each classification.

Detailed definitions for each classification can be found in the Glossary (Section 7), referenced by the red

numbers in each box below. We recommend obtaining tax advice if you think the entity meets one of these

classifications.

5.1. Is the entity an Exempt Beneficial Owner (EBO)?

If you believe the entity does not meet any of the below descriptions, please proceed to Section 5.2.

Exempt Beneficial Owners

Governmental

Organisation

The entity is a

foreign

government or a

government of a

US possession

1

.

W-8BEN-E:

Complete Part

XIII

W-8IMY: n/a

19

International

Organisation

International or

supranational

organisation

whose income

does not benefit

private persons

W-8BEN-E:

Complete Part

XIV

W-8IMY: n/a

20

Central Bank

An institution that

is the principal

authority in issuing

instruments

intended to

circulate as

currency

W-8BEN-E:

Complete Part

XIII

W-8IMY:

Complete Part

XVII

21

Retirement Plan

A fund to provide

retirement benefits

to current or former

employees.

W-8BEN-E:

Complete Part XV

W-8IMY:

Complete Part

XIX

22

Entity wholly

owned by EBOs

Where the equity

interest is owned

by an EBO and

any debt interest

by an EBO or

depository

institution

W-8BEN-E:

Complete Part

XVI

W-8IMY: n/a

23

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

Additional Documentation Requirements

An Entity wholly owned by EBOs must complete a FFI Owner Reporting Statement which can be found at HSBC’s

FATCA website: http://fatca.hsbc.com. In addition, the legislation requires us to obtain documentation from those

owners. HSBC Global Private Bank policy requires this to be the appropriate W-series form to align with existing

bank policies.

1

A possession in this context means American Samoa, Guam, the Northern Mariana Islands, Puerto Rico or the US Virgin Islands

17

5.2. Is the entity a Deemed/ Certified Deemed Compliant Investment Entity?

If you do not consider the entity to be an Exempt Beneficial Owner as set out in Section 5.1, you will need to

consider if the entity meets any of the below registered deemed compliant or certified deemed compliant FFI

classifications. If the entity is an Investment Entity there may be multiple classifications available to it. If you believe

the entity does not meet any of the below descriptions, please proceed to Section 5.3.

Deemed/ Certified Deemed Compliant Investment Entities

Sponsored

Investment Entity

A registered investment

entity whose FATCA

responsibilities are

undertaken by a

sponsor

See 6.2.1 below

Registered Deemed

Compliant or if no

GIIN obtained:

W-8BEN-E: Complete

Part IV

W-8IMY: Complete

Part X

Sponsored Closely

Held Investment

Vehicle

A closely held

investment entity whose

FATCA responsibilities

are undertaken by a

sponsor.

See 6.2.1 below

W-8BEN-E: Complete

Part VII

W-8IMY: Complete

Part XIV

Owner Documented

FFI

An entity that provides

to us details of all

owners and

documentation for these

owners and therefore

does not register.

W-8BEN-E: Complete

Part X

W-8IMY: Complete

Part XI

Qualified Collective

Investment Vehicles

Investment Entities that

are owned solely

through PFFIs or by

large institutional

investors.

Registered Deemed

Compliant

24

25

26

27

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

Additional Documentation Requirements

Owner Documented FFIs must complete a FFI Owner Reporting Statement which can be found at HSBC’s FATCA

website: http://fatca.hsbc.com. In addition, the legislation requires us to obtain documentation from those owners.

HSBC Global Private Bank policy requires this to be the appropriate W-series form to align with existing bank

policies.

Sponsored Entities

There are some classification options where the entity agrees with another entity that it will be its sponsor. By

sponsoring the entity, the sponsor agrees to take on a number of FATCA obligations on its behalf and is likely to

need to register with the IRS.

Should you be interested in a sponsoring arrangement we recommend that you discuss this with the potential

sponsor and obtain tax advice.

HSBC would not generally act as a sponsoring entity except where we are responsible for administering the entity.

18

5.3. Is the entity a Registered or Certified Deemed Compliant Entity?

If you do not consider the entity to meet any the classifications set out in Section 5.1 and Section 5.2 it may fall

into one of the Registered or Certified Deemed Compliant classifications below:

Registered Deemed Compliant

Local FFI

The entity has a local

client base (at least

98% of its accounts are

held by residents of its

country).

Non reporting member

of participating FFI

groups

A Financial Institution

part of a participating

FFI group that

implements procedures

to close/transfer

reportable accounts to

another FI in the group.

Restricted Fund

Entities with prohibitions

on the sale of units in

the fund to specified US

Persons, NPFIs and

Passive NFFEs with

substantial US owners.

Qualified Credit Card

Issuers and Servicers

The entity is an issuer of

credit cards that accept

deposits only when a

customer makes a

payment in excess of a

balance.

28

29

30

31

For the above classifications, complete the Registered Deemed Compliant box on form W-8BEN-E (or W-8IMY if

appropriate).

Certified Deemed Compliant

Local Bank

The entity operates solely as a

bank and has no fixed place of

business outside of its country

of incorporation.

W-8BEN-E: Complete Part V

W-8IMY: Complete Part XII

FFI with only low-value

accounts

For FIs that are not investment

entities that have no accounts

with a value exceeding $50,000

W-8BEN-E: Complete Part VI

W-8IMY: Complete Part XIII

Limited life debt investment

entity

Securitisation companies

created to hold debt until

maturity or until liquidation of the

vehicle

W-8BEN-E: Complete Part VIII

W-8IMY: Complete Part XV

32

33

34

Investment advisors and

managers

Entity must be in the business of

providing investment advice

and/or managing investments

for clients.

W-8BEN-E: Complete Part IX

W-8IMY: n/a

Restricted Distributor

Entity subject to restrictions on

who it can distribute to and

where it can operate

W-8BEN-E: Complete Part XI

W-8IMY: Complete Part XVI

Territory FI

A FI that is not an investment

entity that is organized under

the laws of a possession

1

of the

US

W-8BEN-E: Complete Part

XVII

W-8IMY: Complete Part V

35

36

37

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

1

A possession in this context means American Samoa, Guam, the Northern Mariana Islands, Puerto Rico or the US Virgin Islands

19

6. Is the entity a Non Financial Foreign Entity (NFFE)?

Non-US entities that do not meet any of the Financial Institution (FI) definitions are Non Financial Foreign Entities

(NFFEs). If you have already registered the entity with the IRS as a Direct Reporting NFFE or a Sponsored Direct

Reporting NFFE, please provide the entity’s Global Intermediary Identification Number (GIIN) on the Form W-8BEN-

E or Form W-8IMY (where the entity is an intermediary or flow through entity). It is not necessary for you to continue

through the remainder of this document.

If you have determined that the entity is not a FI, but are unclear what type of NFFE the entity is, please refer to the

below to assist your decision making.

Unless the entity meets any of the below NFFE definitions, it will be a Passive NFFE for the purpose of the

completion of the W-series form and we will require you to provide additional documentation as detailed on

the following page.

20

6.1. NFFEs other than Passive NFFEs

Publicly Traded NFFE

and NFFE affiliates

thereof

The entity’s stock is

regularly traded on an

established securities

market

W-8BEN-E: Complete

Part XXIII

W-8IMY: Complete

Part XXIII

Active NFFE:

<50% Passive Income

Less than half of the

entity’s gross income

and assets are passive.

Passive means derived

from or related to

financial assets

W-8BEN-E: Complete

Part XXV

W-8IMY: Complete

Part XXV

Entity in

liquidation/bankruptcy

The entity was not a FI

in the past 5 years and

is in liquidation or

bankruptcy

W-8BEN-E: Complete

Part XX

W-8IMY: Complete

Part XXII

Excepted Territory

NFFE

An entity organised in a

possession of the US

that does not maintain

financial accounts

W-8BEN-E: Complete

Part XXIV

W-8IMY: Complete

Part XXIV

38

39

40

41

Excepted inter-affiliate

FFI

A FI in a group structure

that does not maintain

accounts for third parties

W-8BEN-E: Complete

Part XXVII

W-8IMY: n/a

Start-up company

The entity is not yet

operating a business

and has no operating

history, but has intent to

operate a non-FI

business.

W-8BEN-E: Complete

Part XIX

W-8IMY: Complete Part

XXI

Non-financial group

entity (holding

company, treasury

center or captive

finance company)

Holds the stock of, or

engages in financing

and hedging

transactions to an entity

that engages in trade

other than that of a FI,

and does not provide

those services to any

non-related entity.

W-8BEN-E: Complete

Part XVIII

W-8IMY: Complete Part

XX

Non-profit or 501(c)

organisation

The entity has been

established for religious,

charitable, scientific,

artistic, cultural or

educational purposes.

NFFEs which do not

meet the glossary

definition may meet the

relevant IGA definition.

An alternative

certification may be

provided in this instance.

W-8BEN-E: Complete

Part XXII or XXI

W-8IMY: N/A

42

43

44

45

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

If you do not believe the entity meets any of the above definitions and it is a not a Financial Institution, then

the entity is likely to be a Passive NFFE. Section 6.2 contains guidance on Passive NFFEs.

21

6.2. Passive NFFEs

Passive NFFE

Entity is not active or a

withholding foreign partnership or

withholding foreign trust for US

Treasury Regulation purposes.

W-8BEN-E: Complete Part

XXVI

W-8IMY: Complete Part XXVI

Sponsored Direct Reporting

NFFE

A registered NFFE where a

sponsor has agreed to report all

direct and indirect substantial US

owners to the relevant authorities.

W-8BEN-E: Complete Part

XXVIII

W-8IMY: Complete Part XXVII

Direct Reporting NFFE

Entity that elects to report

information about its direct or

indirect substantial U.S. owners to

the relevant authorities

W-8BEN-E/W-8IMY: Direct

Reporting NFFE Box

46

47

48

In line with the red reference numbers in each classification box above, detailed definitions have been set out in the Glossary

(Section 7).

Additional Documentation Requirements

Passive NFFEs must complete Part XXVI of Form W-8BEN-E or Form W-8IMY and provide details of substantial

US owners in Part XXX of the Form W- 8BEN-E or on a withholding statement associated with a Form W-8IMY (if

appropriate).

However, in order to align with existing Bank policies HSBC Global Private Bank policy requires an entity customer

to provide additional documentation in respect of any US owner(s) of an entity, i.e., a Form W-9 and, outside the US,

a secrecy waiver. This documentation may already be held on file. If any US Persons are amongst the entity’s

owners we recommend you contact your Relationship Manager to firstly confirm what documentation is already held

on file in respect of these persons. Section 1.1 sets out more detail on ‘US persons’ and required documentation.

Case Study Recap

An entity that does not meet the definition of Financial Institution (Section 3), and does not meet any of the Excepted NFFE

classifications, will be a Passive NFFE.

Examples: Trusts, Personal Investment Companies (PICs), LLCs, and Partnerships that are NOT professionally managed generally

will be considered Passive NFFEs (Section 3.2).

IMPORTANT NOTE: A non-US entity (such as a PIC or trust) that is professionally managed generally will be considered to be an

Investment Entity and therefore a FFI. Such entity may be an Owner Documented FFI, Participating FFI, Reporting Model1 FFI,

Reporting Model 2 FFI, Non Reporting IGA FFI or Nonparticipating FFI.

22

7. Glossary

Below are the model definitions for each FATCA entity classification. These definitions have been taken from the

model IGAs. You should refer to the entity’s local Inter-Governmental Agreement (IGA) or if no IGA is in place, the

US Treasury Regulations, to validate whether there are any local variances.

Key abbreviations used in this document

Abbreviation

EBO

FI

Exempt Beneficial Owner

Financial Institution

IGA

Inter-Governmental Agreement

IRS

Internal Revenue Service

NFFE

Non Financial Foreign Entity

PFFI

Participating Foreign Financial Institution as defined in the US FATCA regulations

(§1.1471-1(b)(91).)

Section 4

Exempt Beneficial Owners

Classification

Requirements

1. Governmental

Organisation

The government of the FATCA Partner or any political subdivision thereof (e.g. state,

county, municipality),

Any wholly owned agency or instrumentality of the FATCA Partner,

Any person, organisation, agency, fund or other body, however designated that

constitutes a governing authority of the FATCA Partner. The net earnings of the

governing authority must be credited to its own or the FATCA Partner accounts with no

portion inuring for the benefit of a private person. This definition does not include any

individual who is a sovereign or official acting in a private capacity,

Any Entity that is separate in form from the FATCA Partner or that otherwise constitutes

a separate juridical entity, provided that:

a. The Entity is wholly owned and controlled by one or more FATCA Partner

Governmental Entities directly or indirectly;

b. The Entity's net earnings are credited to its own or to other FATCA Partner

Governmental Entities with no portion inuring for the benefit of a private person; and

c. Upon dissolution, the Entity's assets vest in one or more FATCA Partner

Governmental Entities.

2. International

Organisation

Any international organisation or intergovernmental organisation or supranational

organisation that:

1. Is comprised primarily of non-US governments;

2. Has in effect a headquarters agreement with a FATCA Partner; and

3. The income of which does not insure to the benefit of private persons

3. Central Bank

An institution that is by law or government sanction the principal authority, other than the

government of [FATCA Partner] itself, issuing instruments intended to circulate as currency.

Such an institution may include an instrumentality that is separate from the government of

[FATCA Partner], whether or not owned in whole or in part by [FATCA Partner].

4. Retirement

Funds

Treaty Qualified

Retirement Fund

A fund established in [FATCA Partner], provided that the fund is entitled to benefits under

an income tax treaty between [FATCA Partner] and the United States on income that it

derives from sources within the United States and is operated principally to administer or

provide pension or retirement benefit.

A fund established in [FATCA Partner] to provide retirement, disability, or death benefits, or

any combination thereof, to beneficiaries that are current or former employees (or persons

designated by such employees) of one or more employers in consideration for services

rendered, provided that the fund:

23

Classification

Requirements

Broad Participation

Retirement Fund

Narrow Participation

Retirement Fund

Pension Fund of

an Exempt

Beneficial Owner

1. Does not have a single beneficiary with a right to more than five percent of the fund’s

assets;

2. Is subject to government regulation and provides annual information reporting about its

beneficiaries to the relevant tax authorities in [FATCA Partner]; and

3. Satisfies at least one of the following requirements:

a. The fund is generally exempt from tax in [FATCA Partner] on investment income

under the laws of [FATCA Partner] due to its status as a retirement or pension plan;

b. The fund receives at least 50 percent of its total contributions from the sponsoring

employers;

c. Distributions or withdrawals from the fund are allowed only if specified events

related to retirement, disability, or death occur (except rollover distributions to other

retirement funds or retirement and pension accounts), or penalties apply to

distributions or withdrawals made before such specified events; or

d. Contributions (other than certain permitted make-up contributions) by employees are

limited by reference to earned income of the employee or may not exceed $50,000

annually.

A fund established in [FATCA Partner] to provide retirement, disability, or death benefits to

beneficiaries that are current or former employees (or persons designated by such

employees) of one or more employers in consideration for services rendered, provided that:

1. The fund has fewer than 50 participants;

2. The fund is sponsored by one or more employers that are not Investment Entities or

Passive NFFEs;

3. The employee and employer contributions to the fund (other than transfers of assets

from treaty-qualified retirement funds described in paragraph A of this section or

retirement and pension accounts described in subparagraph A(1) of section V of this

Annex II) are limited by reference to earned income and compensation of the employee,

respectively.

4. The employee and employer contributions to the fund (other than transfers of assets

from treaty-qualified retirement funds or retirement and pension accounts) are limited by

reference to earned income and compensation of the employee, respectively

5. Participants that are not residents of the FATCA Partner are not entitled to more than

20% of the fund’s assets; and

6. The fund is subject to government regulation and provides information reporting to the

tax authorities in the FATCA Partner.

A fund established in the FATCA Partner by an Exempt Beneficial Owner to provide

retirement, disability, or death benefits to beneficiaries or participants that are:

a. Current or former employees of the Exempt Beneficial Owner (or persons designated by

such employees); or

b. Not current or former employees, if the benefits provided to such beneficiaries or

participants are in consideration of personal services performed for the exempt beneficial

owner.

5. Investment

Entity Wholly

Owned by EBOs

An entity that is a FATCA Partner FI solely because it is an Investment Entity, provided that

each direct holder of:

a. An Equity interest in the entity is an exempt beneficial owner, and

b. Of a debt interest in the entity is either a Depository Institution (with respect to a loan

made to the entity) or an exempt beneficial owner.

24

Investment Vehicles

Classification

Requirements

6. Trustee

Documented

Trust

(Certified-

deemed

compliant)

A trust established under the FATCA Partner's laws to the extent that the trustee is a

Reporting US FI, Reporting Model 1 FFI, or Participating FFI and the trustee reports all the

information required to be reported pursuant to the IGA as would be required if the trust

were a Reporting Financial Institution.

7. Sponsored

Investment

Entity

(Registered-

deemed

compliant)

An Investment Entity established in the FATCA Partner that is not a QI, withholding foreign

partnership, or withholding foreign trust pursuant to US Treasury Regulations, which has a

Sponsoring Entity.

8. Sponsored

Closely Held

Investment

Vehicle

(Certified-

deemed

compliant)

The requirements to qualify as a sponsored closely held investment vehicle are the

following:

The FI must be a FI solely because it is an Investment Entity and is not a US Qualified

Intermediary, withholding foreign partnership or withholding foreign trust;

The FI does not hold itself out as an investment vehicle for unrelated parties, and has

20 or fewer individuals that own its Debt and Equity Interests;

The Sponsoring Entity is a US RFI, Reporting Model 1 FFI or Participating FII and is

authorised to act on behalf of the FI and agrees to perform on its behalf all due

diligence, withholding and reporting responsibilities which would have arisen if the FI

were a RFI;

In addition, the Sponsoring Entity must:

1. Register with the IRS as a sponsoring entity;

2. Agree to undertake all FATCA compliance, withholding and reporting on behalf of the

Sponsored entities;

3. Identify each sponsored FI in all reporting completed on behalf of such sponsored FI;

4. Not have its status as a sponsor revoked.

9. Owner

Documented FFI

(Certified-

deemed

compliant)

An Owner-Documented FFI must meet the following requirements:

Is a FFI solely because it is an investment entity:

Must not be owned by, nor be a member of a group of an expanded affiliated group with

any FI that is a Depository Institution, Custodial Institution or Specified Insurance

Company;

Does not maintain financial accounts for any NPFFIs;

Must provide the required documentation and agree to notify designated withholding

agent which is undertaking the reporting on behalf of the Owner Documented Financial

Institution if there is a change in circumstances.

The FI undertaking obligations on behalf of the Investment Entity must agree to report

the information required on any Specified US Persons but will not need to report on any

indirect owner of the owner documented entity that holds its interest through:

A PFFI;

Model 1 FFI;

Deemed Compliant FI (other than an Owner Documented FI),

Entity that is a US Person,

Exempt Beneficial Owner,

Excepted NFFE.

25

Registered Deemed Compliant

Classification

Definition

10. Collective

Investment

Vehicle

(Registered-

deemed

compliant)

To qualify for this classification, an entity must be a CIV. CIVs are Investment Entities

established in the FATCA Partner and regulated as a collective investment vehicle,

provided that all the interests in the vehicle, including debt interests in excess of $50,000,

are held by or through one or more:

Exempt Beneficial Owners;

Active NFFEs;

US Persons that are not Specified US Persons; or

FIs that are not NPFI.

11. Local Client

Base

A FI that meets the following requirements:

1. The FI must be licensed and regulated as a FI under the FATCA Partner's laws;

2. The FI must have no fixed place of business outside of the FATCA Partner other than a

location that is not publicly advertised and from which the FI performs solely

administrative support functions;

3. The FI must not solicit customers or Account Holders outside the FATCA Partner;

4. The FI must be required under the FATCA Partner's laws to identify resident Account

Holders for purposes of either information reporting or withholding of tax or for satisfying

the FATCA Partner’s AML due diligence requirements;

5. At least 98% of the Financial Accounts by value maintained by the FI must be held by

the FATCA Partner or EU Member State residents (including Entities);

6. On or before 1 July 2014, the FI must implement policies and procedures:

a. To prevent the FI from providing a Financial Account to any NPFI; and

b. To monitor whether the FI opens or maintains a Financial Account for any Specified

US Person who is not a FATCA Partner resident at the time of opening but

subsequently ceases to be a resident of the FATCA Partner or any Passive NFFE

with Controlling Persons who are US residents or citizens not resident of the FATCA

Partner;

7. Such policies and procedures must provide that if any Financial Account held by the

above described persons is identified, the FI must report such account as though the FI

were a RFI or close the account;

8. With respect to a Pre-existing Account held by an individual not resident of the FATCA

Partner or by an Entity, the FI must review those accounts in accordance with the

procedures applicable to Pre-existing Accounts to identify any US Reportable Account or

Financial Account held by a NPFI, and must report such account as though the FI were a

RFI or close the account;

9. Each Related Entity of the FI that is a FI must be incorporated or organized in the

FATCA Partner and, with the exception of any Related Entity that is an Exempt

Beneficial owner retirement fund, meet the same requirements for a Local Client Base

FI; and

10. The FI must not have policies or practices that discriminate against opening or

maintaining Financial Accounts for individuals who are Specified US Persons and

residents of the FATCA Partner.

12. Non reporting

member of

participating FFI

group

A FFI that is a member of a participating FFI group if it meets the following Requirements:

1. By the later of June 30, 2014, or the date it registers with the IRS, the FFI implements

policies and procedures to ensure that within six months of opening a U.S. account or an

account held by a recalcitrant account holder or a nonparticipating FFI, the FFI either

transfers such account to an affiliate that is a participating FFI, reporting Model 1 FFI, or

U.S. financial institution, closes the account, or becomes a participating FFI.

26

Classification

Definition

2. The FFI reviews its accounts that were opened prior to the time it implements the

policies and procedures (including time frames) using the procedures described in

§1.1471-4(c) applicable to preexisting accounts of participating FFIs, to identify any U.S.

account or account held by a nonparticipating FFI. Within six months of the identification

of any account described in this paragraph, the FFI transfers the account to an affiliate

that is a participating FFI, reporting Model 1 FFI, or U.S. financial institution, closes the

account, or becomes a participating FFI.

3. By the later of June 30, 2014, or the date it registers with the IRS, the FFI implements

policies and procedures to ensure that it identifies any account that becomes a U.S.

account or an account held by a recalcitrant account holder or a nonparticipating FFI due

to a change in circumstances. Within six months of the date on which the FFI first has

knowledge or reason to know of the change in the account holder’s chapter 4 status, the

FFI transfers any such account to an affiliate that is a participating FFI, reporting Model 1

FFI, or U.S. financial institution, closes the account, or becomes a participating FFI.

13. Restricted Fund

Investment Entities can obtain Restricted Fund Status where they impose prohibitions on

the sale of units in the fund to specified US Persons, NPFIs and Passive NFFEs with

Controlling US Persons and meet the following requirements:

The FI is an Investment Entity;

The FI is regulated as an investment fund in FATCA Partner and in all of the countries it

is registered and operates;

Interests issued by the fund are redeemed by or transferred by the fund rather than sold

by investors on any secondary market;

Interests not issued by the fund are sold only through distributors that are FIs,

Registered Deemed Compliant FIs, non-registered local banks, or restricted distributors.

The FI prohibits sales or other transfers of Debt or Equity Interests to specified US

Persons, NPFIs and Passive NFFEs with Controlling US Persons;

The prohibition described above must be stated in the FI’s prospectus;

The FI ensures that each distribution agreement requires the distributors to notify any

change of its status within 90 days of the change;

The FI certifies to the Competent Authority with respect to any distributor that ceased to

qualify as a distributor;

The FI reviews the Pre-existing Direct Accounts that are held by the Beneficial Owner of

the interest in the FI in accordance with the procedures applicable to Pre-existing

Accounts;

The FI certifies to the competent authority either that it did not identify any US account

or account held by a NPFI or, in case of such identification, the FI will either redeem or

transfer to an affiliate, a PFI, a Model 1 FI, a US FI, such accounts;

The FI implement the policies in procedures to ensure that it either:

a. Does not open or maintain an account for, or make a withholdable payments to any

specified US Persons, NPFIs and Passive NFFEs with Controlling US Persons and, if

such accounts are discovered, closes all such accounts within 6 months; or

b. Reports on any account held by, or any withholdable payments made to specified US

Persons, NPFIs and Passive NFFEs with Controlling US Persons.

14. Qualified Credit

Card Issuers

and Servicers

To qualify for this classification, a FI must meet the following requirements:

1. The FI is a FI solely because it is an issuer of credit cards that accept deposits only

when a customer makes a payment in excess of a balance due with respect to the card

and the overpayment is not immediately returned to the customer; and

2. On or before 1 July 2014, the FI implements policies and procedures to either prevent a

customer deposit in excess of $50,000, or to ensure that any customer deposit in excess

of $50,000 is refunded to the customer within 60 days. Customer deposits do not include

credit balances in relation to disputed charges but include credit balances resulting from

merchandise returns.

27

Certified Deemed Compliant

Classification

Requirements

15. Local Bank

FIs that are licensed and regulated by the FATCA Partner's laws and operate as a bank or a

credit union or similar cooperative credit organisation that is operated without profit.

They must meet the following requirements:

1. The FI’s business consists primarily of receiving deposits from and making loans to, with

respect to a bank, unrelated retail customers and, with respect to a credit union or similar

cooperative credit organisation, members, provided that no member has a greater than

5% interest in such credit union or cooperative credit organisation;

2. The FI must have no fixed place of business outside of FATCA Partner other than a

location that is not publicly advertised and from which the FI performs solely

administrative support functions;

3. The FI must not solicit customers or Account Holders outside FATCA Partner;

4. The FI must not have more than $175m in assets on its balance sheet and not more than

$500m in total for a group of Related Entities;

5. Any Related Entity and any Related Entity that is a FI must be incorporated or organized

in the FATCA Partner and, with the exception of any Related Entity that is an Exempt

Beneficial owner retirement fund or a FI with only low-value accounts, meet the same

requirements described above.

16. FFI with only

low-value

accounts

A FI that meets the following requirements:

1. The FI is not an Investment Entity;

2. Each Financial Account maintained by the FI or any Related Entity must not exceed

$50,000 taking into account aggregation and currency translation;

3. The FI must not have more than $50m in assets on its solus balance sheet (and its

consolidated balance sheet where it is in a group) at the end of its most recent accounting

year.

17. Limited life

debt

investment

entity

Special Purpose Vehicles created to hold debt until maturity or until liquidation of the vehicle

will be regarded as Certified Deemed Compliant FI.

To qualify for this transitional relief the securitisation vehicle must:

Have been established prior to 17 January 2013; and

Meet the definition of a securitisation company set out in FATCA Partner's laws.

18. Investment

Advisors and

Managers