Combined

and/or

carve-out

financial

statements

IFRS application guidance

April 2017

Contents

Important note 1

About this publication 2

1 Introduction to combined and/or carve-out

financial statements 4

1.1 Types of financial information 4

1.2 Objective of combined and/or carve-out

financial statements 7

1.3 Combined vs carve-out financial statements 7

1.4 Types of transactions for which combined

and/or carve-out financial statements are

prepared 10

2 Boundaries of the reporting entity 13

2.1 Fit for purpose 13

2.2 Step 1: Are the components under common

control? 15

2.3 Step 2: Are all relevant economic activities

included? 17

3 Overall approach to preparing the financial

statements 22

3.1 Overview 22

3.2 Commonly observed overall approaches 27

3.3 Disclosure of accounting policies 30

3.4 Continuity of financial information 31

4 Accounting policies and estimates 35

4.1 Implications of a separate combined/

carved-out reporting entity 35

4.2 Accounting treatment for related party

transactions in combined and/or carve-out

financial statements 36

4.3 Estimates and compliance with IFRS 42

4.4 Consolidation procedures 44

4.5 Statement of financial position 44

4.6 Statement of profit or loss and OCI 49

4.7 Equity 53

4.8 Other allocation and presentation issues 53

5 Disclosures 62

5.1 Boundaries of the reporting entity 62

5.2 Overall approach to preparing the financial

statements 67

5.3 Accounting policies and estimates 70

6 Practical considerations 75

6.1 Project management 75

6.2 IT systems and data gathering 76

6.3 Central and shared services 78

6.4 Supporting documentation 79

6.5 Involvement of other functions 79

6.6 Internal controls 80

6.7 Audit and reporting considerations 80

Acknowledgements 83

Keeping in touch 84

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Important note

What’s the issue?

Users and regulators often require companies to provide combined and/or carve-

out financial statements because they can provide meaningful, relevant and

usefulinformation.

But answers to questions about combined and/or carve-out financial statements

have not always proven to be intuitive and/or consistent around the globe.

This makes the preparation of combined and/or carve-out financial statements

challenging processes that require considerable judgement by management.

Why is there diversity

in practice?

There isn’t a specific IFRS that deals with combined and/or carve-out financial

statements, so local practices have developed, often through discussions

withregulators.

How will this

This guidance aims to highlight practice where IFRS is applied consistently globally.

guidance help?

It also aims to draw attention to those areas in which we have observed diversity in

the application of IFRS.

General-purpose

financial statements

Combined and/or carve-out financial statements may be considered general-

purpose financial statements. However, there is a distinction between them and

other general-purpose financial statements, such as financial statements of a

legal entity or of an existing group. To make the distinction clear in this publication,

general-purpose financial statements of a legal entity or of an existing group are

referred to as ‘generic financial statements’.

This terminology is not acknowledged in IFRS, but is used solely to make the

distinction clear and prevent repetition in this practical guide.

Areas of application

issues

This symbol highlights areas in which heightened awareness may

be required; we recommend you consult your KPMG professional.

For these areas, we describe an approach(es) that we think would be more

consistent with the principles of IFRS applied to generic financial statements,

and highlight other approaches seen in practice.

Given the fact that IFRS does not address combined and/or carve-out financial

statements, we recognise that in practice the application of accounting

treatments for combined and/or carve-out financial statements may vary

between jurisdictions. Some of the approaches we describe in this publication

may be inappropriate based on specific regulatory requirements and/or would

not be observed in practice in certain jurisdictions.

This publication has not been developed in contemplation for any specific

jurisdiction or regulatory environment and therefore, we recommend

consultation with your KPMG professional to understand the accepted

practice(s) in your jurisdiction and any applicable local regulatory requirements

orrestrictions.

2| Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

About this publication

Scope

The purpose of this publication is to provide guidance on the preparation of

combined and/or carve-out financial statements that are based on historical data

and prepared in accordance with IFRS.

As at April 2017, this material reflects our latest thinking and observations on this

topic globally. The guidance in this publication is mainly based on our experience

of the practice that has developed in applying IFRS to combined and/or carve-out

financial statements in relation to relevant sections from Insights into IFRS.

Combined and/or carve-out financial statements that are not prepared in

accordance with IFRS are not in the scope of this publication – e.g. those prepared

in accordance with US GAAP or SIR 2000 Investment Reporting Standards

Applicable to Public Reporting Engagements on Historical Financial Information

inthe UK.

Definition

In this publication, we generally use the term ‘combined and/or carve-out

financial statements’ as a generic term meaning: a set of historical financial

information comprising one or more economic activities that can be objectively

distinguished from other economic activities within the larger reporting entity.

These activities are typically under common control, do not comprise an existing

legal entity or group and are presented as a single reporting entity.

This definition is supported by the fact that, although there is no specific guidance

in the standards, the IASB has long acknowledged the principle that combined

financial statements can comply with IFRS. For example, the IFRS for SMEs defines

combined financial statements as ‘a single set of financial statements of two or

more entities controlled by a single investor’ (paragraph 9.28).

This sentiment is reinforced by commentary included in the IASB’s May 2015

exposure draft Conceptual Framework for Financial Reporting, which proposes

the following definition of combined financial statements: ‘financial statements

prepared for two or more entities that do not have a parent-subsidiary relationship’

(paragraph3.17). The accompanying basis for conclusions observes that combined

financial statements may provide useful information in some circumstances,

but that developing guidance on how to apply IFRS in such statements would

be best undertaken in a project specific to that topic (paragraph3.17 of the basis

for conclusions). The definition proposed in the exposure draft encompasses

the concept of carve-out financial statements, and is broader than the working

definition used in this publication.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Combined vs carve-out

financial statements

The terms ‘combined financial statements’ and ‘carve-out financial statements’

areoften used interchangeably, or one or the other term is used exclusively in a

certain jurisdiction.

For some combined financial statements – i.e. financial statements that represent

the combination of two entities owned by the same individual – there is no larger

reporting entity and therefore no financial information for a larger reporting entity

available. However, the absence of a larger reporting entity does not in itself prevent

a set of combined financial statements from being in compliance with IFRS.

For a further discussion of what distinguishes the two types of financial statements

in some jurisdictions, seeChapter1.3.

Regulatory

r

equirements

This publication is not intended to address regulatory requirements in specific

jurisdictions, although some examples are included for illustrative purposes.

Therefore, it should also be used in conjunction with any relevant regulatory

requirements.

Organisation of the text

References are included in the left-hand margin of this guide. Where relevant, the

text is referenced to source material – primarily IFRS and the 13th edition 2016/17 of

our publication Insights into IFRS, but also SEC pronouncements in some cases.

CF.OB2 Paragraph 2 of chapter ‘Objective of general purpose financial

reporting’ in the Conceptual Framework for Financial Reporting.

IAS 1.82(a) Paragraph 82(a) of IAS 1 Presentation of Financial Statements.

SEC FRM 7410 Section 7410 of the Financial Reporting Manual of the Division of

Corporation Finance of the SEC.

Insights 2.3.60.10 Paragraph 2.3.60.10 of the 13th Edition 2016/17 of Insights

intoIFRS.

Abbreviations

The following abbreviations are used throughout this publication.

COSO Committee of Sponsoring Organisations

FRM Financial Reporting Manual of the Division of Corporation Finance of the

SEC, which provides general guidance about SEC financial reporting and

filing matters

IPO Initial public offering

ISA International Standard on Auditing

ISAE International Standard on Assurance Engagements

M&A Mergers and acquisitions

Newco A newly formed entity, used to describe the entity that is formed and

continues in existence post-transaction (if any)

OCI Other comprehensive income

SEC US Securities and Exchange Commission

About this publication |

3

4|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1 Introduction to combined

and/or carve-out financial

statements

1.1 Types of financial information

Financial information can be retrospective (past-looking) or prospective

(forward-looking). Retrospective financial information is generally classified

as either historical or pro forma. Historical information is based solely on past

transactions or events. In contrast, pro forma information aims to illustrate how a

consummated or proposed transaction (or event) might have affected the financial

information presented in a prospectus or other document had the transaction

occurred at an earlier date. Pro forma financial information does not represent a

company’s actual financial position or results – it addresses a hypothetical situation

and is prepared for illustrative purposes only.

Offering documents, both regulated and unregulated, often include both types of

information.

Combined

and/or

carve-out

Stand-alone

and

consolidated

Retrospective

Prospective

Types of financial information

Pro forma

Historical

Projections

Forecasts

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Type of information Description

IAS 27.4

HISTORICAL

Stand-alone

financial

statements

A set of financial statements prepared for an

individual legal entity, which are a structured

representation of the financial position and

financial performance of the entity. Referred to as

‘separate’ financial statements by a parent that has

one or more subsidiaries.

IAS 27.4

Consolidated

financial

statements

A set of financial statements prepared for a group

in which the assets, liabilities, equity, income,

expenses and cash flows of the parent and its

subsidiaries are presented as those of a single

economicactivity.

Combined and/or

carve-out financial

statements

A set of historical financial information comprising

one or more economic activities that can be

objectively distinguished from other economic

activities within the larger reporting entity (if there

is one). These activities are typically under common

control, and do not comprise an existing legal entity

or group but are presented as a single reporting

entity (seeChapter1.2).

ISAE 3420

Pro forma Financial information shown together with

adjustments to illustrate the impact of an event or

transaction on unadjusted financial information as

if the event had occurred or the transaction had

been undertaken at an earlier date selected for the

purposes of the illustration.

ISAE 3400

Forecast Prospective financial information prepared on

the basis of assumptions about future events

that management expects to take place and the

actions that management expects to take as at the

date the information is prepared (best-estimate

assumptions).

ISAE 3400

Projection Prospective financial information prepared on the

basis of:

– hypothetical assumptions about future

events and management actions that are not

necessarily expected to take place; or

– a mixture of best-estimate and hypothetical

assumptions.

This information illustrates the possible

consequences as at the date the information is

prepared if events and actions were to occur (an

‘as-if’ or ‘what-if’ scenario).

1 Introduction to combined and/or carve-out financial statements

5

1.1 Types of financial information

6|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

This publication focuses on the preparation of combined and/or carve-out financial

statements that are based on historical data. A combined/carved-out reporting

entity includes components that historically ‘belonged’ together during all periods

presented. For a more detailed discussion on determining the boundaries of the

reporting entity, see Section 2.

Example 1A – Historical vs pro forma financial information

Group R operates in the retail sector. On 1 July 2016, R acquires the retail

operations of Group V.

Group V’s historical financial statements for the retail operations

For the purpose of presenting the operations that are being disposed of to R,

V prepares carve-out financial statements for the year ended 30 June 2016

that comprise only its retail operations. These financial statements are in effect

a subset of V’s consolidated financial statements – they present historical

financial information about V’s retail operations.

Group R’s pro forma financial information

To illustrate the effect of the acquisition of V’s retail operations, R prepares the

following pro forma financial information as at 30 June 2016:

– a pro forma statement of profit or loss and OCI for the six months ended

30June 2016 that includes V’s retail operations from 1January to 30 June

2016 as if they had been acquired on 1January 2016; and

– a pro forma statement of financial position as at 30 June 2016 that includes

V’s retail operations as at 30 June 2016 as if they had been acquired on

30June 2016.

Group R’s historical financial information

R prepares consolidated financial statements over 2016, which include the

retail operations as from the date of acquisition. The consolidated financial

statements represent historical financial information.

The following diagram highlights the distinction between the historical and pro

forma financial information in this example.

Group V’s

retail operations

Group R + Group V’s

retail operations

1 January 2016

Group R + Group V’s

retail operations

Group R

31 December 20

16

1 July 2016

Date of acquisition

Group V’s historical

financial statements

for its retail operation

Group R’s historical

consolidated financial

statements

Group R’s pro forma

financial information

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1.2 Objective of combined and/or carve-out financial

statements

CF.OB2, QC1–QC30 If financial information is to be useful to investors, lenders and other creditors,

then it needs to be relevant and faithfully represent what it purports to

represent. Its usefulness is enhanced if it is comparable, verifiable, timely

and understandable. However, because combined and/or carve-out financial

statements are not currently defined in IFRS, and IFRS does not provide any

specific guidance on their preparation,

1

significant judgement is needed, based on

the purpose for which the financial statements are being prepared, to ensure that

they meet the objective of providing useful information.

Combined and/or carve-out financial statements provide financial information about

one or more of the economic activities that are part of a larger reporting entity. We

have observed that the components of these statements can include subsidiaries,

divisions, branches and/or an aggregation of all similar assets, associated liabilities

and operations in a specified geographic region or line of business. They may

have separate management and accounting records, but they could also have

management, expenses and other resources in common with other components

of the larger reporting entity. The components are typically under common control

for all periods presented (seeChapter2.2).

1.3 Combined vs carve-out financial statements

The appropriate identification and labelling of a set of financial statements as either

‘combined’ or ‘carve-out’ may depend on the jurisdiction. In jurisdictions that make

a distinction between the terms, the difference usually arises from the nature of

the individual components from which the financial statements aredrawn.

– Combined financial statements:The combination of two or more legal entities

or businesses that may or may not be part of the same group, but do not

by themselves meet the definition of a group under IFRS10 Consolidated

Financial Statements – i.e. a parent and all of its subsidiaries. At a simplistic

level, preparing combined financial statements involves adding together two or

more legal entities and eliminating any inter-company transactions – e.g. inter-

company profits, revenue and expenses, receivables and payables and equity

(e.g. unrealised gains and losses).

– Carve-out financial statements: Financial statements that include one or more

components that are parts of a larger reporting entity. The term ‘carve-out’

reflects the fact that smaller components – e.g. unincorporated businesses such

as divisions – are being carved out from a larger reporting entity.

1. The IASB’s May 2015 exposure draft Conceptual Framework for Financial Reporting included

a definition of combined financial statements. The IASB’s staff summary of January 2017

showed that the definition has not changed in the course of the Board’s redeliberations on

the exposure draft. However, the revised Conceptual Framework has not been finalised and

therefore is not effective yet.

1 Introduction to combined and/or carve-out financial statements

7

1.3 Combined vs carve-out financial statements

8|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 1B – Combined financial statements

Owner B has three separate businesses comprising separate legal entities

that each prepare stand-alone financial statements. B ‘combines’ the stand-

alone financial statements into a single set of combined financial statements in

preparation for an IPO.

Owner B

Cable TV, LLC

Telephone, LLC

Internet, LLC

Example 1C – Carve-out financial statements

Owner D has a cable and telephone business that is part of a single legal entity.

D ‘carves out’ the cable division into a set of carve-out financial statements in

preparation for an IPO.

Owner D

Cable TV

Division

Telephone

Division

Telecoms, LLC

Combined and carve-out financial statements are not mutually exclusive. As the

following example illustrates, it is common to have elements of both. In these

cases, the financial statements might also be referred to as ‘combined and carve-

out’ financial statements.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 1D – Combined and carve-out financial statements

Group X operates across a number of jurisdictions, with interests in both

clothing and furniture. X wishes to carve out and sell its clothing division in an

IPO, and is required by regulation to prepare combined and carve-out financial

statements for the clothing operations.

As the following diagram illustrates, this involves combining clothing operations

from Jurisdictions J and K owned by Subsidiary S1 and carving out a portion of

Subsidiary S2.

Clothing:

Jurisdiction K

Furniture

Division

Clothing

Division

Clothing:

Jurisdiction J

Subsidiary S1

(Retail)

Subsidiary S2

(Retail)

Group X

The following table describes the characteristics that are usually found in

combined or carve-out financial statements when a distinction is made.

Factor

Combined

financial

statements

Carve-out

financial

statements

Chapter

Based on historical

financial information

Ye s Ye s 1. 1

Consists solely of

whole legal entities

Ye s Generally,

no – consists

of smaller

components of a

larger reporting

entity

1. 3

Typically under

common control

throughout the period

being reported on

Ye s Ye s 2.2

1 Introduction to combined and/or carve-out financial statements

9

1.3 Combined vs carve-out financial statements

10 |

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Factor

Combined

financial

statements

Carve-out

financial

statements

Chapter

Each component has

its own (separate)

accounting records

and processes that

have enabled it in

the past to prepare

stand-alone financial

statements

Ye s Generally, no.

However, certain

financial metrics

– e.g. revenue,

operating profit,

net income – may

have generally

been tracked

historically for

internal reporting

purposes

2.3

The entities could

operate as stand-

alone businesses with

little or no assistance

from the parent

entity/owners

Generally, yes Generally, no –

need additional

support from

parent/owners

4.1

Extent of allocations

necessary to

prepare the financial

statements

Allocations

generally not

pervasive

Allocations vary 4.2

and

4.3

1.4 Types of transactions for which combined and/or

carve-out financial statements are prepared

IFRS financial statements are frequently used in capital market transactions to

present the economic activities of an issuer in a prospectus. However, in many

cases the issuer’s legal structure is changed and customised specifically for the

planned transaction. As a result, historical financial information based on the

legal entity or existing group may not be sufficient to appropriately represent the

economic activities of the reporting entity that will be formed after the transaction.

In these circumstances, it is often required or desirable to prepare another type of

historical financial information instead: financial statements based on an economic

perspective. The objective of combined and/or carve-out financial statements is

to present aggregated historical financial information of components that have

not in the past represented a reporting entity. These financial statements may be

necessary to facilitate various transactions, including:

– an IPO: e.g. for a group of divisions;

– a spin-off: e.g. of a group of divisions; or

– private M&A transactions: i.e. acquisitions and disposals, for either (net) asset(s)

or share deals.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1.4.10 Required by regulation

In many jurisdictions, combined and/or carve-out financial statements are required

or permitted by regulation. The following are examples.

– The EU Prospectus Regulations set out a framework for the preparation

and publication of a single prospectus throughout Europe. This means that

a prospectus approved in one country may be used in another. However, it

leaves responsibility for the implementation of detailed regulations to the

memberstates.

In accordance with the EU Prospectus Directive, an issuer may be required by a

national authority to present combined and/or carve-out statements when it:

– makes an offer to the public of shares;

– issues other transferable securities equivalent to shares or other securities

that can be converted;

– exchanges transferable equivalent securities into shares under certain

circumstances; or

– asks for the admission of its securities to trading on a regulated market.

The same applies to the issue of debt, although there are no explicit legal

requirements. Nonetheless, in some situations combined and/or carve-out

financial statements may be useful for someinvestors.

– In the US, combined and/or carve-out financial statements have been prepared

for decades for the purposes of capital market transactions based on regulatory

requirements. Common scenarios include IPOs that are arranged as ‘put-

together transactions’ or ‘roll-up transactions’ for which either SEC FormS-1

or F-1 is filed with the SEC. In put-together transactions, two or more parties

transfer net assets to a Newco in exchange for shares in that reporting

entity; in roll-up transactions, an investor (usually from the private equity

or alternative investment sector) acquires two or more smaller businesses

from the same sector and merges them into a Newco. The SEC has issued

several pronouncements that address combined and/or carve-out financial

statements for these scenarios. In addition, for the purpose of ad hoc reporting

in conjunction with significant acquisitions by SEC registrants in accordance

with SEC Regulation S-X 3-05, combined and/or carve-out financial statements

prepared on the basis of IFRS might be reported under certain circumstances.

– In Hong Kong, it is common practice for companies seeking a listing to carry

out a reorganisation of the proposed combined and/or carved-out listed

components before listing. Under the Hong Kong Listing Rules, all listing

candidates have to present historical financial statements of the proposed

combined and/or carved-out listing components for the track record period.

If the reorganisation takes place after the end of the track record period and

involves a Newco acquiring companies or businesses that, together with the

Newco, are held under common control and form the proposed combined or

carved-out listing group, then the historical financial statements are normally

presented on a combinedbasis.

– In Canada, in accordance with the Companion Policy to National

Instrument41-101 (General Prospectus Requirements), the financial

statements of the primary business of the issuer have to be provided. The

‘primary business’ typically includes the newly acquired significant acquisition,

which is generally reflected in combined and/or carve-out situations. This

1 Introduction to combined and/or carve-out financial statements

11

1.4 Types of transactions for which combined and/or carve-out financial statements are prepared

12|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Companion Policy references the guidance in the Companion Policy to National

Instrument 51-102 (Continuous Disclosure Obligations) for the requirements on

combined and/or carve-out basis financial statements.

– In Mexico, under the Mexican National Banking and Securities Commission

Rules, all companies seeking a listing on the Mexican Stock Exchange have

to present historical financial statements of the proposed combined and/or

carved-out listing components for the relevant required periods (i.e. three years

of historical financial statements). If the reorganisation of the legal entities or

combined and/or carved-out components takes place before or simultaneously

with the IPO transaction, then the historical financial statements are normally

presented on a combined/carved-out basis.

1.4.20 Unregulated

Private contracts in connection with M&A transactions are among the most

common scenarios for which combined and/or carve-out financial statements are

prepared. These include, for example, sales of a part of a business in the form

of controlled auctions or private placements. These transactions may take place

outside the regulatory environment if the entities involved are not subject to

regulatory requirements – e.g. because neither of the entities has shares traded

on public markets.

In some jurisdictions, mostly within the EU and US, an entity can also issue

financial instruments in private placements on non-regulated ‘open markets’, which

in contrast with a public offering or the admission of securities to trading on a

regular market, might not be subject to regulatory review. However, combined

and/or carve-out financial statements might still be included for the business(es)

subject to the transaction.

The following are other examples of unregulated transactions for which combined

and/or carve-out financial statements might be prepared.

– A bank issues a loan to legal entities within a group that is secured by asset

pledges or guarantees. In addition to a set of consolidated financial statements

prepared by the parent, the bank may request combined and/or carve-out

financial statements for the subgroup of legal entities of the group that actually

receive the loan.

– Individuals (or members of a family) could personally hold majority interests in

two or more entities, so that these interests are not bundled in a group holding

entity that would be required to prepare consolidated financial statements.

These individuals may be interested to receive financial information on a

combined basis.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Boundaries of the reporting

entity

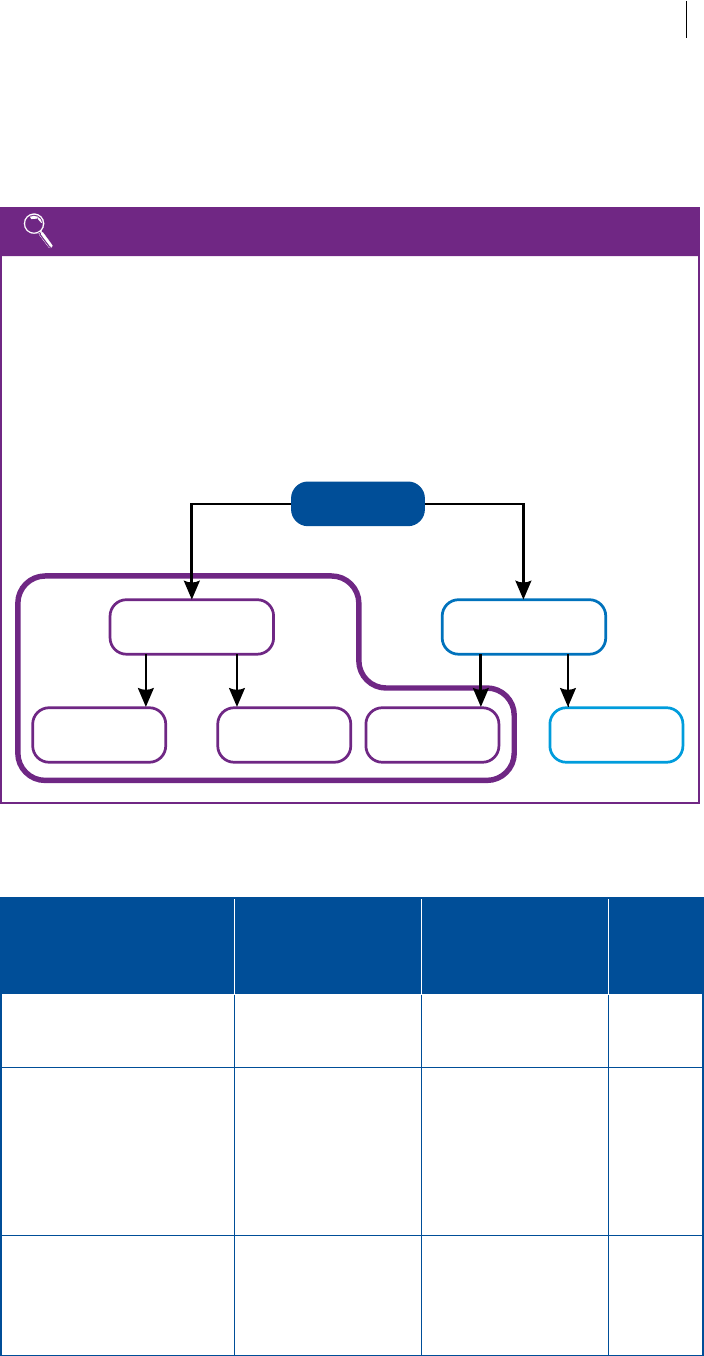

2.1 Fit for purpose

In preparing combined and/or carve-out financial statements, the reporting entity

is tailored to meet the specific purpose for which the financial statements are

being prepared, and does not have to constitute an existing legal entity or group;

it may become a legal entity or group on completion of the transaction (if there

is one). Therefore, the determination of the boundaries of the reporting entity for

combined and/or carve-out financial statements can be complex and often requires

more judgement than for generic financial statements.

To determine the boundaries, management needs to consider the overarching

question of whether the combined and/or carve-out financial statements are

fit for the intended purpose. This question underlying the determination of the

boundaries of the reporting entity is essential because it is the decisive element

in whether information is useful to potential and existing investors, lenders

andregulators (where applicable).

To be fit for purpose, the combined and/or carve-out financial statements need

to portray the reporting entity consistently with the purpose for which they

are prepared. This may depend on a variety of aspects, including the following

qualitative factors:

– the reason why the financial statements are being prepared;

– the information intended to be conveyed;

– the expected users;

– consistency of the combined/carved-out reporting entity with the post-

transaction reporting entity (particularly in the case of an IPO); and

– the markets in which the financial statements will be released and the related

legal and regulatory requirements.

In determining whether it is practicable for management to prepare combined and/

or carve-out financial statements that comply with IFRS, management assesses

the extent to which the entity is able to separate each component’s financial

performance and assets/liabilities from those of the larger reporting entity (see

Chapter 4.3).

The following are two key elements that management needs to consider, in

addition to the qualitative factors set out above, when determining whether

the boundaries of a reporting entity are set so that they will result in financial

statements that are fit for purpose.

1. Are the components under common control during the reporting period

included in the combined and/or carve-out financial statements?

2

2. Are all relevant activities included?

2. These transactions are typically under common control; however, other practices have been

observed. See Chapter 2.2 for more guidance.

2 Boundaries of the reporting entity

13

2.1 Fit for purpose

14|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Fit for

purpose*

Are the components

under common control?

(Chapter 2.2)

Are all relevant activities

included?

(Chapter 2.3)

This diagram is a paradigm (i.e. not considered to be a mathematical formula). Whether the

combined/carved-out reporting entity is fit for purpose depends on a variety of aspects,

including qualitative factors, the two key elements included and other relevant aspects.

*

Note

Although all factors are relevant in a variety of cases, the assessment is typically

more straightforward when the combined and/or carve-out financial statements:

– are included in a registered offering and the related regulations have specific

requirements for their content; or

– are being used to effect a private M&A transaction on the basis of a (draft) purchase-

and-sale agreement and the components of the financial statements are identified

on the basis of defined economic characteristics.

Although there is no specific guidance on determining the boundaries of a

reporting entity, the following terms that are used in IFRS may be useful in

determining the boundaries of the reporting entity based on the purpose of the

financial statements.

Te rm Definition

Legal entity

There is no formal definition of what constitutes a legal

entity under IFRS, and definitions may vary by jurisdiction.

However, a legal entity generally has a legally enforceable

ability to enter into a contractual agreement and assume the

obligations necessary to operate a business or engage in start-

up operations. Legal entities can take various forms, including

corporations, partnerships, joint ventures, proprietorships

andtrusts.

IFRS 3.A

Business**

An integrated set of activities and assets that is capable of

being conducted and managed for the purpose of providing a

return in the form of dividends, lower costs or other economic

benefits directly to investors or other owners, members or

participants.

IFRS 10.A

Group

A parent and its subsidiaries.

IFRS 10.A

Subsidiary

An entity that is controlled by another entity (i.e. its parent).

IFRS 10.A

Consolidated

financial

statements

Financial statements of a group in which the assets, liabilities,

equity, income, expenses and cash flows of the parent and

its subsidiaries are presented as those of a single economic

activity.

IAS 27.4

Separate

financial

statements

Financial statements presented by a parent or an investor with

joint control of, or significant influence over, an investee. An

entity is allowed to choose one of the following accounting

policies to account for interests in subsidiaries, associates and

joint ventures, unless they are classified as held-for-sale:

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Te rm Definition

Separate

financial

statements

(continued)

– at cost;

– using the equity method as described in IAS 28 Investments

in Associates and Joint Ventures; or

– in accordance with IAS 39 Financial Instruments:

Recognition and Measurement.

IFRS 5.32

Discontinued

operations

A component of an entity that either has been disposed of or is

classified as held-for-sale and:

– represents a separate major line of business or geographic

area of operations;

– is part of a single co-ordinated plan to dispose of a separate

major line of business or geographic area of operations; or

– is a subsidiary acquired exclusively with a view to resale.

IFRS 8.5

Operating

segment

A component of an entity:

– that engages in business activities from which it may earn

revenues and incur expenses (including revenues and

expenses relating to transactions with other components of

the same entity);

– whose operating results are regularly reviewed by the

entity’s chief operating decision maker to make decisions

about resources to be allocated to the segment and assess

its performance; and

– for which discrete financial information is available.

IAS 36.6

Cash-

generating

unit

The smallest identifiable group of assets that generates cash

inflows that are largely independent of the cash inflows from

other assets or groups of assets.

Note

** In June 2016, the IASB published the exposure draft Definition of a Business and

Accounting for Previously Held Interests – Proposed Amendments to IFRS 3 and IFRS11.

The proposed amendments aim to provide clearer application guidance to distinguish

between a business and a group of assets when applying IFRS 3 Business Combinations

and how an entity should account for a previously held interest in a business, if acquiring

control or joint control of that business.

2.2 Step 1: Are the components under common control?

In order to prepare combined and/or carve-out financial statements, all

components included in the combined and/or carve-out financial statements

are typically under common control throughout the entire reporting period(s)

presented.

Insights 5.13.10.10 A ‘business combination involving entities or businesses under common control’

is a business combination in which all of the combining entities or businesses

are ultimately controlled by the same party or parties both before and after

the combination, and that control is not transitory.

Further guidance on what

constitutes common control is included in 5.13.10 in Insights into IFRS.

2 Boundaries of the reporting entity

15

2.2 Step 1: Are the components under common control?

16|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

IFRS 3.B1 For generic financial statements, the application of any guidance on common

control is restricted to entities under common control and not extended further

to entities under common management. However, we have observed that in

practice, in limited circumstances and in certain jurisdictions, combined and/or

carve-out financial statements are being presented for entities under common

management. These financial statements include entities that were not under

common control but were under common management for all periods presented

in the financialstatements.

The determination of whether combined and/or carve-out financial statements

for entities under common management are appropriate is a matter of judgement

taking into account the purpose of the financial statements and any regulatory

requirements, as well as whether there is a rational basis for their preparation and

the need to ensure that the information conveyed by the financial statements is

not misleading.

We recommend that you research common practice in your jurisdiction, to ensure

that you understand the predominant practice in the jurisdiction, because the

boundaries of the reporting entity may differ significantly depending on whether

the application of a common management rationale is appropriate.

Management

company

Company C Company D

Owner W: 50%

Owner X: 50%

Owner Y: 60%

Owner Z: 40%

Example 2A – Common management: Family members

Members of a family own two companies. Two family members own Company

C, which operates in the retail sector. Two different family members own

Company D, which also operates in the retail sector but in a different city in the

samecountry.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

All of the day-to-day decisions for both companies are made by the family

management company, and decisions made by the management company affect

both companies. The management company does not consolidate C and D.

The family members plan to list a Newco that will hold the shares in C and D.

For this purpose, the family plans to prepare combined financial statements that

include both companies. In this example, it may be reasonable to conclude that

common management, without common control, is a sufficient basis on which

to prepare combined financial statements, assuming that the other criteria are

met (see Chapter2.1).

For further discussion of when family relationships result in common control,

see 5.13.10.40–50 in Insights into IFRS.

For an example of the basis of preparation of a set of combined and/or carve-

out financial statements prepared on the basis of common management, see

Disclosure 5C in Section 5.

2.3 Step 2: Are all relevant economic activities included?

Combined and/or carve-out financial statements comprise one or more economic

activities that can be objectively distinguished from other economic activities

within the larger reporting entity. There is no specific definition of ‘economic

activities’ in IFRS, and a final determination will depend on regulations in the

relevant jurisdiction and/or the judgement of management assessed against the

purpose for which the financial statements are being prepared. This assessment

includes whether the appropriate assets, associated liabilities and operations have

been included in each component of the reporting entity, as well as an assessment

of whether the combined and/or carve-out financial statements are complete.

Whether it is appropriate to include or exclude components from combined and/

or carve-out financial statements often depends on whether the purpose of the

financial statements is to display management’s track record. For example, for

an IPO without a change in management (i.e. the same management before and

after the IPO for the business being carved out), information on management’s

track record may be relevant and useful for investors; therefore, the inclusion of all

relevant activities may be necessary. Conversely, for a private M&A transaction in

which a seller and buyer of identified economic activities have determined in the

purchase-and-sale agreement the exact net assets to be transferred, the combined

and/or carve-out financial statements typically exclude activities and related

assets and liabilities that will not be transferred to thebuyer. The track record of

management may not be relevant in this circumstance.

In some cases, the approach elected depends on the requirements of specific

laws or regulations, or the views of regulators, in the jurisdiction(s) in which an

offering document will be filed or the transaction is taking effect.

Being able to isolate economic activities for the purpose of preparing the financial

statements is important for a final determination of whether the financial

statements can comply with IFRS (seeChapter4.1) and whether they are fit for

the intended purpose.

2 Boundaries of the reporting entity

17

2.3 Step 2: Are all relevant economic activities included?

18|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Given that the determination of whether all relevant economic activities are

included is highly dependent on the specific facts and circumstances, no specific

approach can be prescribed. However, based on our general observations the

following factors are used in practice to assess whether economic activities can

be distinguished for the purpose of preparing a set of combined and/or carve-out

financial statements.

Factor General observation

Independent

cash inflows

Generally, an economic activity has independent cash

inflows, which are separate and distinct from other streams

of cash inflows and might be a factor to distinguish the

economic activity.

Shared assets

Different sets of economic activities have limited shared

assets, other than shared facilities such as a corporate office.

For example, if a single piece of equipment is used to

produce two similar products, then the economic activities

may not be distinguished, even if the two products have

independent cash inflows. In this example, the equipment is

being used for the same general purpose.

Common costs

There are minimal shared costs between different sets of

economic activities. Distinct economic activities have no

more than incidental common facilities and costs.

Management

The day-to-day activities of different sets of economic

activities are managed independently of one another – i.e.

each economic activity has historically been managed as if it

were autonomous.

Nature of

product or

service

A set of economic activities can be distinguished by the type

of end product or service, use of the product or service,

customer base, pricing, costs and/orbrand.

Geography

Geography is not generally a factor in determining the scope

of an economicactivity.

Post-combined

operations

After the transaction for which the combined and/or carve-

out financial statements are being prepared, dissimilar

economic activities will be operated, managed and financed

separately.

The above factors are guidelines with no particular weighting, and as such are not

intended as ‘bright lines’. Consideration of the above factors will vary, depending

on the purpose for which the combined and/or carve-out financial statements are

being prepared.

See examples of the disclosure of the economic activities that are included in the

combined/carved-out reporting entity in Chapter 5.1.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 2B – Management’s track record

Company C has 50 health clubs that operate under a recognisable brand with

operations throughout Country Y. The health clubs are all owned and managed

centrally by the company and all operate under the same criteria – i.e. all have

the same theme, fitness classes, price structure, prime locations, customer

base etc. The health clubs and central management comprise one legal entity.

Of the 50 health clubs, 10 have historically been loss-making whereas the

other 40 have been extremely successful. The reasons for the 10health clubs

underperforming vary and can be attributed in part to competition and poor on-

site management.

Company C

Loss-

making

(10)

Health clubs

Profitable

(40)

C plans to raise additional capital to allow for expansion of the business both in

and outside Y via an IPO through a spin-off. C plans to list only the 40successful

health clubs, which will be transferred to a Newco ahead of theIPO.

For the purposes of the IPO, management is required by local regulations to

prepare a set of carve-out financial statements that provide investors with

information to evaluate the strength of the brand and the overall track record of

management. The financial information intended to be conveyed in the carve-out

financial statements is the historical financial performance of all clubs. As such,

the reporting entity to be included in the carve-out financial statements will

include all relevant activities that have been a part of the history of the business

and that can be expected to continue as the business after the IPO.

2 Boundaries of the reporting entity

19

2.3 Step 2: Are all relevant economic activities included?

20|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

The assessment of common control as outlined in Step 1 concludes that

common control exists. The following factors are used to assess how the

business is run and whether all relevant activities are included.

Independent cash

inflows

Each health club has independent cash inflows.

Shared assets

The health clubs do not have shared assets.

Common costs

The health clubs have minimal shared costs.

Management

The health clubs have central management,

which results in the clubs being operated by the

same management team.

Nature of product or

service

The health clubs have the same theme, fitness

classes, price structure, prime locations,

customer base etc.

Post-combined

operations

After the IPO, the 40 successful health clubs will

be managed separately from the 10 loss-making

health clubs.

In this example, the economic activities of the 10 unsuccessful health clubs

cannot be distinguished from those of the 40 successful health clubs. All of

the health clubs are under the same brand, offer the same products and are

operated by the same management team. The carve-out financial statements

intend to portray the historical financial performance of all clubs. Therefore,

in consultation with the regulator, management concludes that excluding

the 10unsuccessful health clubs would not provide useful information to the

financial statement users about management’s track record because it would

not include all relevant activities.

Accordingly, management concludes that it would be inappropriate for the

reporting entity to include only the successful health clubs and exclude the

unsuccessful health clubs. Such an approach would not provide more relevant

information to financial statement users going forward, because it cannot be

expected that all new health clubs will be successful.

For a discussion of the presentation and measurement of components of

combined and/or carve-out financial statements that will not be part of the

business going forward – e.g. the 10 unsuccessful health clubs in this example

– see 4.8.10.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

We understand that some regulators, in similar circumstances, specifically

require the exclusion of the operations that will not be part of the business

going forward. Applying this requirement in the example above, the carved-out

reporting entity would include only the 40 successful health clubs and exclude

the loss-making operations.

This approach would not be consistent with the application of IFRS to generic

financial statements. We recommend that you research common practice in

your jurisdiction before proceeding with combined and/or carve-out financial

statements that exclude economic activities that cannot be distinguished from

the operations that are included in the combined/carved-out reporting entity, to

understand accepted practice in the jurisdiction.

2 Boundaries of the reporting entity

21

2.3 Step 2: Are all relevant economic activities included?

22|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Overall approach to

preparing the financial

statements

3.1 Overview

The chosen overall approach should be appropriate for the purpose of the

financial statements. This chapter provides an overview of the overall approaches

commonly used to prepare combined and/or carve-out financial statements.

Globally, several approaches have been observed that have been applied to

combined and/or carve-out financial statements. Although not all of them

are consistent with the principles of IFRS for generic financial statements,

all described approaches may have some technical merit for the purposes of

combined and/or carve-out financial statements, depending on the specific facts

and circumstances.

In general, there are two key decisions that management needs to make about the

overall approach before preparing combined and/or carve-out financial statements:

– whether the combined/carved-out reporting entity will be a first-time adopter

of IFRS and, if yes, how IFRS1 First-time Adoption of International Financial

Reporting Standards will be applied; and

– whether the combined and/or carve-out financial statements will be extracted

from the consolidated financial statements of the larger group (if a larger

group exists) to which the combined/carved-out reporting entity belongs (top-

down approach) or built up from the financial statements of the entities or

components that are being combined or carved out (bottom-up approach).

Although the primary decision is typically whether to use a top-down or bottom-up

approach, these decisions are not independent, which means that management’s

decision-making process can be complex. A more in-depth discussion follows

in Chapter 3.2, providing background information that is relevant to deciding on

theapproach.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

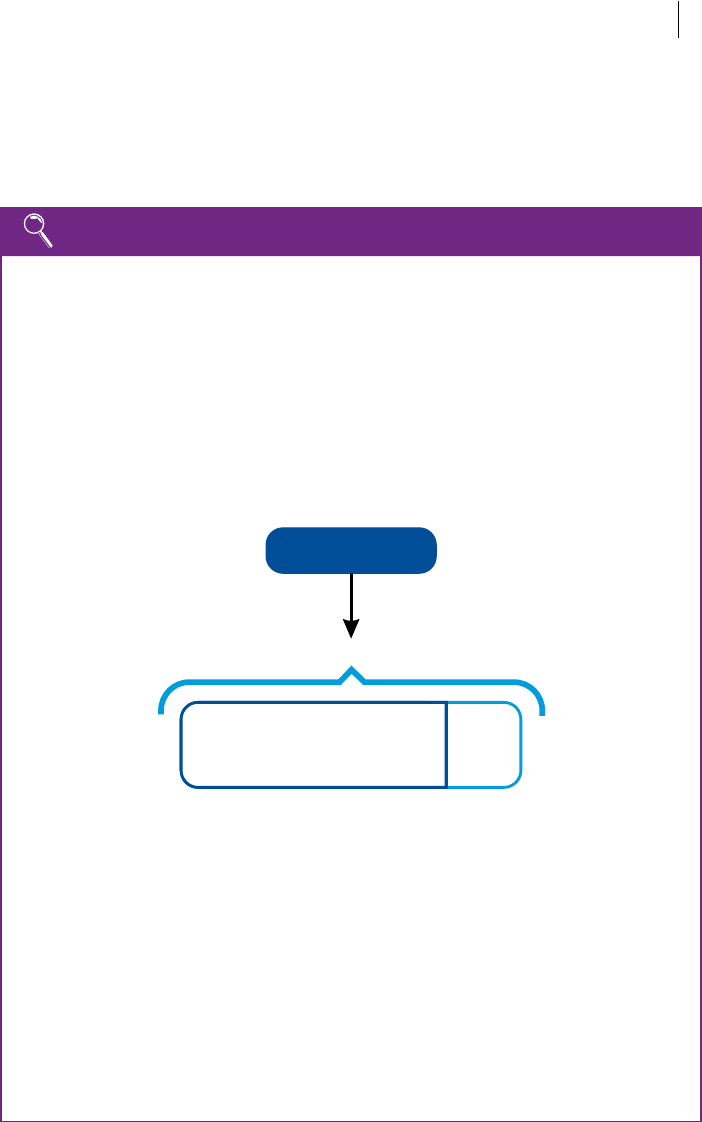

3.1.10 The application of IFRS 1

An entity is required to apply IFRS 1 in its first IFRS financial statements – these

are the first annual financial statements in which the entity adopts IFRS by an

explicit and unreserved statement of compliance with IFRS. Guidance on the

application of IFRS1 is contained in Chapter 6.1 of Insights into IFRS and is not

repeated here except for the issues discussed below.

References in this publication to an entity that prepares its financial statements

in accordance with IFRS mean an entity that also distributes those financial

statements to the entity’s owners or any other external parties – i.e. it has adopted

IFRS as envisaged in IFRS1.

The following example highlights the key terms used in applying IFRS1.

Example 3A – Key terms on first-time adoption

Company X plans to present its first IFRS financial statements for the year

ended 31December 2016 – i.e. X will be a first-time adopter of IFRS in 2016.

X will present one year of comparative information. The following diagram

illustrates the key dates and periods in relation to X’s adoption of IFRS.

1 January 2015

Date of transition/

opening IFRS

statement of

financial position

31 December 2015 31 December 2016

First annual

IFRS

reporting date

First IFRS financial

statements/first IFRS

reporting period

IFRS comparatives

In this diagram, X is presenting only one year of comparative information on the

basis of IFRS, and therefore has a date of transition of 1January 2015.

IFRS requires comparative information to be presented for at least one previous

reporting period, but does not prohibit the presentation of more than one year

of comparative information. The first-time adopter’s date of transition is at the

start of the earliest comparative period presented on the basis ofIFRS.

In our experience, there is diversity over whether the combined/carved-out

reporting entity is considered to be a first-time adopter of IFRS. In some

jurisdictions, a combined/carved-out reporting entity is always considered to be a

first-time adopter of IFRS because this entity did not previously issue IFRS financial

statements. Accordingly, the combined and/or carve-out financial statements are

the combined/carved-out reporting entity’s first IFRS financialstatements.

Ho

wever, we have also observed in other jurisdictions that a combined/carved-out

reporting entity is treated as a part of the larger reporting entity, which has already

issued IFRS financial statements. Therefore, because the combined/carved-out

reporting entity is already reflected under IFRS in the financial statements of the

larger reporting entity, it is not considered to be a first-time adopter.

3 Overall approach to preparing the financial statements

23

3.1 Overview

24|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Presentation and disclosure

IFRS 1.6, 21 An entity’s first IFRS financial statements include presentation of the opening

statement of financial position. Therefore, an entity in its first IFRS financial

statements presents at least three statements of financial position:

– as at the first annual IFRS reporting date;

– as at the previous annual reporting date; and

– as at the date of transition.

Example 3B – Complete set of financial statements under IFRS1

Continuing Example 3A, Group X’s carve-out financial statements for the year

ended 31December 2016 comprise the following primary statements.

Statement of profit or loss

and OCI

Statement of changes

in equity

Statement of cash flows

Statement of profit or loss

and OCI

Statement of changes

in equity

Statement of cash flows

1 January 2015 31 December 2015 31 December 2016

Statement of

financial position

Statement of

financial position

Statement of

financial position

Comparatives: Current period:

In addition to presenting a third statement of financial position as at the date

of transition, IFRS1 also requires the presentation of ‘related notes’. This

requirement should be interpreted as requiring disclosure of those notes that are

relevant to an understanding of how the transition from previous GAAP to IFRS

affected the first-time adopter’s financial position at the date of transition – i.e.

not all notes related to the opening statement of financial position are required in

every circumstance.

Insights 6.1.1540.20 A first-time adopter might approach its decision about the relevant note

disclosures by first assuming that all notes are necessary and then considering

which note disclosures are not relevant to an understanding of the effect of

the transition to IFRS and may be omitted. In deciding which notes and other

comparative information to omit, the entity considers materiality and the particular

facts and circumstances of the first-time adopter, including legislative and other

requirements of the jurisdiction in which the first-time adopter operates.

Guidance on the presentation and disclosure relevant to a first-time adopter of

IFRS is included in Chapter 6.1 in Insights into IFRS.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Reconciliations

IFRS 1.23–25 Extensive disclosures are generally required in an entity’s first IFRS financial

statements to explain how the transition from previous GAAP to IFRS affected the

reported financial position, financial performance and cash flows of the first-time

adopter. These disclosures include reconciliations of equity and reported profit

or loss at the date of transition and at the end of the latest period presented

in the entity’s most recent annual financial statements in accordance with

previousGAAP.

IFRS 1.28 These reconciliations are not required in combined and/or carve-out financial

statements if there are no equivalent financial statements that have been

published under previous GAAP for the reporting entity with which the IFRS

financial statements can be compared.

3.1.20 Top-down vs bottom-up approaches

The following examples explain the concepts of the top-down and bottom-up

approaches.

Example 3C – Top-down approach

Group X is a consumer markets group that is planning an IPO to sell its clothing

operations, which are partly held in two subsidiaries and partly held in a division

that is not a separate legal entity. As part of the mandatory listing documents for

the planned IPO, X will prepare carve-out financial statements for the clothing

operations.

Clothing:

Jurisdiction K

Furniture

Division

Clothing

Division

Clothing:

Jurisdiction J

Subsidiary S1

(Retail)

Group X

Subsidiary S2

(Retail)

X decides to prepare the financial statements by extracting the financial

information for the clothing operations from its consolidated financial

statements – i.e. a top-down approach. This means that the carrying amounts

recognised by the larger reporting entity in its consolidated financial statements

for the clothing operations will be included in the carve-out financial statements.

3 Overall approach to preparing the financial statements

25

3.1 Overview

26|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 3D – Bottom-up approach

Group Z holds an extensive portfolio of investment properties in Country Y.

Each property is held in a separate company (Subsidiaries S1 to S50), which

has independent operations and prepares its own financial statements. Z also

prepares consolidated financial statements.

Z intends to list three of its subsidiaries (S1–S3) in an IPO of a new real estate

investment trust (REIT). As part of the preparation for the IPO, Z transfers the

shares in the related companies to a Newco.

Investors

Sub S2 Sub S3Sub S1

Group Z

Sub S2

Sub S3

Sub S1

Subs

S4–S50

BeforeAfter

REIT

Newco

Holdco 1 Holdco 2

As part of the listing documents, Z is required to present combined financial

statements for the three property companies (sometimes referred to as the

‘underlying financial statements’).

Z decides to prepare the financial statements by combining the financial

statements of Subsidiaries S1, S2 and S3 – i.e. a bottom-up approach. This

means that any effects from applying acquisition accounting at the level of

S1, S2 or S3 (i.e. to the extent that any of these subsidiaries have their own

subsidiary-investees) will be retained in the combined financial statements.

However, any effects from applying business combination accounting at the

level of Holdco1 or Holdco 2 are not carried over into the combined reporting

entities, regardless of how they have been kept for bookkeeping or other

internal purposes in the past.

In determining whether to use the top-down or bottom-up approach, it is

necessary to consider whether IFRS financial statements from the larger reporting

entity are available. They might be available because the larger reporting entity has

issued financial statements in compliance with IFRS.

Further, management needs to consider the requirements or preferences of any

relevant regulator, common practice in the region or jurisdiction in which the

combined and/or carve-out financial statements will be filed or used and other

available relevant information.

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3.2 Commonly observed overall approaches

This chapter outlines approaches to preparing combined and/or carve-out financial

statements that in our experience are commonly used.

3.2.10 focuses on the approaches used if the combined/carved-out reporting entity

is considered to be a first-time adopter of IFRS, and 3.2.20 describes the overall

approaches if it is not considered a first-time adopter of IFRS.

The approaches discussed here are those most commonly seen in practice.

Werecommend researching common practice in your jurisdiction before selecting

an approach.

3.2.10 Combined/carved-out reporting entity is a first-time adopter

of IFRS

Around the globe, the following approaches are the most common for a combined/

carved-out reporting entity that is considered a first-time adopter of IFRS.

The two approaches use the guidance in paragraph D16 of IFRS 1 for the

combined/carved-out reporting entity when a subsidiary becomes a first-time

adopter later than its parent.

IFRS 1.D16 The combined/carved-out reporting entity is treated as the subsidiary mentioned

in paragraph D16, and the guidance in paragraphs D16(a) or D16(b) is applied to it.

This means that the subsidiary may measure its assets and liabilities at the date of

transition at either:

IFRS 1.D16(a) – the amounts included in the consolidated financial statements of the parent,

based on the parent’s date of transition, excluding the effects of consolidation

procedures and the business combination in which the parent acquired the

subsidiary; or

IFRS 1.D16(b) – the carrying amounts required by IFRS1 based on the subsidiary’s own date of

transition.

In some cases, there might be no difference between these two approaches,

because there are no adjustments recorded in the consolidated financial

statements of the parent.

The following paragraphs discuss these approaches in more detail.

Financial statements prepared applying paragraph D16(a) of IFRS 1

To apply paragraphD16(a) of IFRS 1 to combined and/or carve-out financial

statements, the larger reporting entity needs to have issued IFRS-compliant

financial statements.

IFRS 1.D16(a) When using paragraph D16(a), the relevant IFRS financial information for the

combined/carved-out reporting entity is extracted from the financial statements

of the larger reporting entity. The combined and/or carve-out financial statements

are based on the parent’s date of transition excluding the effects of consolidation

procedures and the business combination in which the parent acquired the

subsidiary – e.g. goodwill.

However, it has been observed that some combined and/or carve-out financial

statements following this approach include the effects of the business combination

in which the parent acquired the subsidiary that is a component of the combined

and/or carve-out reporting entity, including goodwill. The rationale for including the

goodwill is that an exclusion of goodwill or fair value adjustments would lead to

an incomplete set of financial statements for the combined/carved-out reporting

3 Overall approach to preparing the financial statements

27

3.2 Commonly observed overall approaches

28|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

entity, because they would not reflect all of the costs and resources controlled

by the business. If the goodwill were excluded from the combined/carved-out

reporting entity, then the combined and/or carve-out financial statements may not

be as relevant and/or useful for the users of the financial statements.

This approach would be considered inconsistent with IFRS for generic financial

statements.

Example 3E – Financial statements prepared applying

paragraphD16(a) of IFRS 1

Modifying Example 3C, Group X concluded that it would prepare the carve-out

financial statements for its clothing operations applying paragraph D16(a).

X has previously prepared and issued consolidated financial statements in

accordance with IFRS, which include the clothing operations. The clothing

division in Jurisdiction J was acquired in 2014. From the purchase price

allocation of this acquisition, goodwill is recognised in X’s consolidated financial

statements.

The carve-out financial statements for the year ended 31December 2016,

with 2015 comparative information, are based on the same carrying amounts

as the IFRS consolidated financial statements of X, excluding the effects of

consolidation procedures and the goodwill that arose as part of the business

combination in which X acquired the clothing division.

The carve-out financial statements include all of the presentation and

disclosures required by IFRS1, except that no reconciliation to previous GAAP

is presented (see 3.1.20).

The guidance included in Insights into IFRS Chapter 6.1 is applicable.

If the larger reporting entity did not issue IFRS-compliant financial statements,

then paragraph D16(a) of IFRS 1 is not available. However, we have observed in

practice that management might use the following approach to prepare combined

and/or carve-out financial statements.

In the initial step, the larger reporting entit

y prepares consolidated financial

statements that comply with IFRS applying IFRS 1 without issuing the prepared

financial statements (i.e. the larger reporting entity does not become an IFRS

adopter). In the second step, management extracts the information from the

consolidated financial statements to prepare the combined and/or carve-out

financial statements. In this second step, management therefore essentially

applies paragraph D16(a) to the internally produced IFRS financial statements.

This approach is inconsistent with the application of paragraphD16(a) for the

purposes of generic financial statements.

Financial statements prepared applying paragraph D16(b) of IFRS 1

IFRS 1.D16(b) The second possibility is to prepare combined and/or carve-out financial

statements in accordance with IFRS 1 by building them up based on the entity’s

own date of transition. This approach follows paragraph D16(b) of IFRS 1, if the

larger reporting entity has already issued IFRS-compliant financial statements.

Under this approach, management applies the requirements of IFRS 1,

including the mandatory exceptions, and may apply the optional exemptions

provided by IFRS1. This approach requires the combined/carved-out reporting

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

entity to determine its IFRS 1-compliant amounts for the financial statements

without considering the carrying amount of the larger reporting entity’s assets

andliabilities (see Disclosure5G in Section5).

Example 3F – Financial statements prepared applying

paragraphD16(b) of IFRS 1

In Example 3D, Group Z concluded that it would prepare the combined financial

statements applying paragraph D16(b).

None of the companies in Z has previously prepared its financial statements in

accordance with IFRS; instead, they have all applied local GAAP.

To prepare the combined financial statements, Z follows these steps.

Step 1 Each of Subsidiaries S1, S2 and S3 prepares IFRS financial

information that complies with IFRS for the year ended

31December 2016, with a date of transition of 1January

2015.

This step is necessary in order to create the base data

for the preparation of combined financial statements that

comply with IFRS.

1

Step 2

The combined financial statements for the year ended

31December 2016, with 2015 comparative information,

are created by combining the IFRS financial information

prepared in respect of S1, S2 and S3.

For simplicity, this example assumes that S1, S2 and

S3 have consistent accounting policies. However, if this

were not the case then they would have to be aligned in

preparing the combined financial statements.

The combined financial statements include all of the presentation and

disclosures required by IFRS1, except that no reconciliation to previous GAAP

is presented (see3.1.20).

The guidance included in Chapter 6.1 of Insights into IFRS is applicable.

Note

1. Step 1 does not, in itself, make any of S1, S2 or S3 a first-time adopter of IFRS. To be a

first-time adopter, a complete set of financial statements would need to be prepared,

they would need to include an explicit and unreserved statement of compliance with

IFRS and they would need to be distributed to external parties (see3.1.20).

3.2.20 Combined/carved-out reporting entity is not a first-time

adopter of IFRS

In our experience, there are two overall approaches that are most common for a

combined/carved-out reporting entity that is not considered a first-time adopter

of IFRS. Under the first approach, the financial information is extracted from the

larger reporting entity (top-down approach), whereas under the second approach

the financial information is based on the components of the combined/carved-out

reporting entity (bottom-up approach).

3 Overall approach to preparing the financial statements

29

3.2 Commonly observed overall approaches

30|

Combined and/or carve-out financial statements

© 2017 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Financial information is extracted from the larger reporting entity (top-

down approach)

Under the top-down approach, financial information is extracted from the larger

reporting entity’s consolidated financial statements in order to prepare the

combined and/or carve out financial statements. The assets and liabilities are

extracted from the larger reporting entity and the combined/carved-out reporting

entity continues to apply the same accounting policies.

Under this approach, the information in the combined and/or carve-out financial

statements is considered a part of the IFRS financial statements for the larger

reporting entity because financial information about the economic activities that

are included in the combined/carved-out reporting entity is already reflected in the

(consolidated) financial statements of the larger reporting entity. Therefore, the

financial information can be extracted from the (consolidated) financial statements