S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

1

Chapter 4 – Financial Management

Table of Contents

4.1 Financial Management 4-4

4.2 Responsibilities 4-4

4.2.1 Commanding Officer 4-4

4.2.1.1 Actions 4-5

4.2.2 Comptroller 4-6

4.2.3 Accountable Officials 4-7

4.3 Fiscal Law and Regulations 4-8

4.3.1 Purpose, Time and Amount 4-8

4.3.2 Anti-Deficiency Act Violation Reporting 4-9

4.3.3 Anti-Deficiency Act Violation Penalties 4-9

4.4 Types of Appropriations 4-10

4.4.1 Appropriations 4-10

4.4.1.1 Operations & Maintenance, Navy (O&M,N) 4-10

4.4.1.2 Operations & Maintenance, Naval Reserve (O&M,NR) 4-10

4.4.1.3 Shipbuilding and Conversion, Navy (SCN) 4-11

4.4.1.4 Weapons Procurement, Navy (WPN) 4-11

4.4.1.4.1 Other Procurement, Navy (OPN) 4-11

4.4.1.5 Research, Development, Test and Evaluation (RDT&E) 4-11

4.4.1.6 Navy Working Capital Fund (NWCF) 4-12

4.4.1.7 Foreign Military Sales (FMS) 4-12

4.4.1.8 National Defense Sealift Funds (NDSF) 4-12

4.5 Budgeting and Accounting 4-12

4.5.1 SUPSHIP Mission Budgets 4-12

4.5.2 Navy Enterprise Resource Planning (Navy ERP) 4-13

4.5.2.1 Roles in ERP 4-14

4.5.2.2 ERP Site Leads 4-14

4.5.3 The Standard Accounting and Reporting Systems (STARS) 4-14

4.6 Purpose of Funds Provided to SUPSHIPs 4-15

4.6.1 SUPSHIP Mission Funds 4-15

4.6.2 Ship Construction Funds 4-15

4.6.3 Foreign Military Sales (FMS) Funds 4-16

4.6.4 Ship Repair Funds 4-16

4.6.5 Fleet Modernization Program (FMP) Funds 4-17

4.6.6 Berthing Funds 4-17

4.6.7 Commander Naval Installations (CNI) Funds 4-18

4.6.8 Environmental Compliance Oversight Funds 4-18

4.6.9 Reimbursable Work Orders (RWO) 4-19

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

2

4.7 Funding Methods 4-19

4.7.1 Mission Funding Allotment 4-19

4.7.2 Reimbursable Orders 4-19

4.7.2.1 Types of Reimbursable Orders 4-20

4.7.2.1.1 Project Order (PO) 4-20

4.7.2.1.2 Economy Act Order (EAO) 4-20

4.7.3 Military Interdepartmental Purchase Request (MIPR) 4-21

4.7.4 Direct Citations 4-21

4.7.5 Budget Structure WBS Elements from ERP Activities 4-22

4.8 General Classifications of Funds Transactions 4-22

4.9 Prompt Payment Act, 5 CFR 1315 4-23

4.9.1 Progress Payments and Prompt Payment Requirements 4-23

Chapter 4 Acronyms 4-25

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

3

References

(a) SECNAVINST 7000.27C, Comptroller Organizations

(b)

DoD 7000.14-R, DoD Financial Management Regulation

(c)

SECNAVINST 5200.35G, DoN Managers’ Internal Control (MIC) Program

(d)

31 USC 3528, Responsibilities and Relief from Liability of Certifying Officials

(e)

Public Law 104-106 Section 913

(f)

31 USC 1301(a), Application

(g)

31 USC 1502, Balances Available

(h)

31 USC 1341, Limitations on Expending and Obligating Amounts

(i)

31 USC 1342, Limitation on Voluntary Services

(j)

31 USC 1517, Prohibited Obligations and Expenditures

(k)

31 USC 1349, Adverse Personnel Actions

(l)

31 USC 1350, Criminal Penalty

(m)

31 USC 1518, Adverse Personnel Actions

(n)

31 USC 1519, Criminal Penalty

(o)

NAVSO-P 1000, DoN Financial Policy Manual

(p)

OMB Circular A-123, Management’s Responsibility for Enterprise Risk Management and

Internal Controls

(q)

Standards of Internal Control in the Federal Government (“Green Book”), GAO-14-704

(r)

10 USC 7572, Quarters: Accommodations in Place of for Members on Sea Duty

(s)

Assistant Secretary of the Navy, (Financial Management and Comptroller)

(ASN(FM&C)) memo dated 3 May 2002

(t)

41 USC 23, Orders or Contracts for Material Placed with Government-owned

Establishments Deemed Obligations

(u)

31 USC 1535, Agency Agreements

(v)

Public Law 104-134, Debt Collection Improvement Act of 1996

(w)

5 CFR 1315, Prompt Payment Act (PL 97-177)

Figures

Figure 4-1: SUPSHIP Funding Decision Tree .................................................................... 4-24

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

4

Chapter 4 – Financial Management

Financial Management

A command’s program for the proper administration of funds is an integral part of effective

management. There are specific responsibilities associated with managing public funds

which go to the highest levels of SUPSHIP organizations. The goal of this chapter is to

explain the importance of proper financial management within the SUPSHIPs and with their

customers. This chapter will refer to overarching guidance for Financial Management in the

Department of Defense. The actual references rather than this volume should be consulted

and used to make policy decisions with legal/financial implications. For the Department of

the Navy, SECNAVINST 7000.27

C, Comptroller Organizations, reference (a), is the authority

and provides guidance for the establishment, periodic reviews and approval of Comptroller

organizations. This directive assigns responsibility to the commanding officer for ensuring

the command has a financial management organization capable of proper and effective

administration of funds and complying with applicable laws, regulations, policies, procedures,

and sound financial practices.

Key to achieving this objective is an understanding of the integration of budgeting,

accounting and performance measurement while adhering to the legislative requirements for

financial management in the Federal Government.

Responsibilities

Commanding Officer

The Supervisor of Shipbuilding, as commanding officer, has specific responsibilities with

regard to Financial Management. Commanding officers of activities that receive a sub

allocation of funds from a Navy or Marine Corps organization are responsible under

31 USC

1341 and 31 USC 1517 for the proper administration of all funds received. They are required

to have a qualified Comptroller, to delegate authority to that Comptroller for the appropriation

accounts involved, and to designate specific responsibilities for the authority delegated. The

Comptroller can then delegate authority and/or signature authority for funding documents to

other individuals within the Comptroller organization. All delegations of authority must be

documented in writing and maintained for audit. In addition, commanding officers are

responsible for establishing and maintaining internal control systems to ensure that:

• All available funds are identified, controlled and recorded in the official accounting

records from the time received until subdivided to others or obligated and expended.

• All available funds are identified with authorized purposes by account and period of

availability for new obligations and period of availability for expenditures.

• All special and recurring provisions and limitations on the obligation and expenditure of

funds are identified and documented for all available funds and accounts.

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

5

• All proposed obligations of funds are reviewed to ensure that sufficient funds are

available to cover the obligations, that the purpose of the obligations is consistent with

the authorized purposes of the funds or accounts, and that the obligation does not violate

any special or recurring provisions and limitations on the incurrence of obligations.

• These internal control requirements apply to all appropriations and funds provided to the

command by apportionments, allocations, allotments, reimbursable orders, or other

means.

• All documents associated with financial transactions are well-documented and

accessible per guidance contained in DoD 7000.14-R

, DoD Financial Management

Regulation (DoD FMR), reference (b), and to ensure commands are audit ready.

The proper stewardship of federal resources is a fundamental responsibility of command.

These internal control requirements apply to all appropriations and funds provided to the

command. Further guidance can be found in SECNAVINST 7000.27C and SECNAVINST

5200.35G, DoN Managers’ Internal Control Program (MICP), reference (c).

4.2.1.1 Actions

Commanding officers are obligated to take all necessary actions to establish accountability

and enhance the administrative control of funds, including:

• Hiring a qualified Comptroller and establishing an organizational structure which provides

unfettered access and a direct reporting chain from the Comptroller to the commanding

officer.

• Establishing and maintaining adequate fiscal controls to prevent over-authorization, over-

commitment, over-obligation, or over-expenditure of funds made available to the activity.

Prompt reporting of any violation is also required.

• Issuing an activity instruction providing for the authority, responsibility, and procedures

required in the administrative control of funds.

• Delegating funds administration authority to individuals in the Comptroller organization at

the appropriate level to ensure that the individuals are personally aware of the necessary

detail to establish total accountability. These funds administrators should be in a position

that enables them to provide approval or disapproval of financial transactions. Overall

financial management remains the responsibility of the activity Comptroller.

• Ensuring that subordinates delegated the authority to act as funds administrators are

authorized in writing, by name, clearly specifying the extent of the authority.

• Ensuring that delegated funds administrators are familiar with the statutory

responsibilities inherent in the administration of funds.

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

6

Comptroller

The Comptroller is the senior financial manager within the SUPSHIP command and the chief

financial advisor to the Supervisor. Responsibility for the command’s financial management

and integrity is inherent in this position. The Comptroller shall ensure that the requirements

of DoD FMR are met. In addition, the Comptroller will establish a system of internal controls

to ensure all government resources are used efficiently and effectively to achieve intended

program results, consistent with applicable laws and regulations, and in a way that minimizes

the potential for waste, fraud and mismanagement.

As referenced in enclosure (1) of SECNAVINST 7000.27C

, the Comptroller organization has

overall responsibility for financial management in six major functional areas:

• Budget Formulation includes those actions performed in development, review,

justification, and presentation of budget estimates and requires organizations consider

expected demand and the resources required to meet that demand. The focus is on

prioritizing these requirements and requesting adequate resources to achieve the highest

priorities in each year. It also creates a baseline against which actual results can be

compared.

• Budget Execution encompasses those budgetary actions required to effectively and

efficiently accomplish the programs for which funds were requested and appropriated.

The process must ensure funds are administered in accordance with applicable laws,

administrative policies and regulations of higher authority.

• Managerial Accounting concepts and standards are aimed at providing reliable and

timely information on the full cost of programs. It involves establishing accounting control

over assets provided to the command and the accumulation and preparation of financial

information on a regular basis for analysis and decision-making.

• Program Analysis is the process of identification, measurement, analysis, interpretation,

and communication of financial information. This information is used by management to

plan, evaluate, make decisions, and improve operational efficiency within an organization

and assure appropriate use of, and accountability for, its resources.

• Performance Measurement is the process of tying financial data to results. It

emphasizes objectively assessing operational performance and effectiveness using

valid, identifiable criteria; analyzing data, information and results; identifying trends and

deviations; and projecting future outcomes to guide programmatic decision-making and

risk management. Because it measures progress towards achievement of goals and

objectives, it is also a long-term planning tool that can justify resource allocation.

• Audit Readiness is a state of being prepared at all times to demonstrate proper manual

and automated processes and documentation (e.g. process controls, financial controls,

Information Technology (IT) controls) that are executed in accordance with policy and

appropriate accounting standards. SUPSHIPs can maintain a constant state of audit

readiness by having business processes that are sustainable, traceable and repeatable.

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

7

Inherent in the Comptroller’s responsibilities are the requirements to:

• Guard against inadvertent or deliberate violations of statute or regulation

• Ensure prompt recording of authorizations, commitments and obligations in budgetary

accounts

• Monitor the recording of assets, liabilities and expenses in proprietary accounts

• Monitor the processes of pre-validation and certification of payments

• Review outstanding commitments and obligations to ensure they are valid

• Match disbursements to obligations and accounts payable

• Issue and accept funding documents which obligate direct appropriations, working capital

or customer funds

• Ensure timely billing of costs incurred against funding documents and the prompt

matching of collections associated with those billings

• Certify completeness and accuracy of those transactions included in financial statements

and reports prepared by the Defense Finance and Accounting Service (DFAS) on behalf

of the activity

Accountable Officials

An accountable official is a member of the military or a DoD civilian to whom public funds are

entrusted or who participates in the process of certifying vouchers for payment. Individuals

who are delegated authority by the commanding officer to authorize, commit, obligate, and

expend specific funds related to a specified authority and responsibility are agents of the

Comptroller.

Comptroller personnel are responsible for certifying fund availability and assignment of

proper funding citations on commitment and obligating documents. However, a certification

of fund availability is not a certification for payment. A Departmental Accountable Official

(DAO) is a government employee who participates in the process of certifying vouchers for

payment. Certifying officers and DAO are both considered accountable officials. Certifying

officers ensure transactions are properly documented and computed correctly according to

source documents and that they are correct and proper for payment.

CERTIFYING OFFICERS: Certifying officers must have knowledge, background or

experience in the preparation of a voucher for payment. In support of voucher certifications,

they must check the accuracy of facts stated on a voucher and, in supporting documentation,

verify the computation and determine the legality of a proposed payment. All certifying

officers must have completed an approved certifying officer legislation training course

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

8

applicable to their mission area within two weeks of their appointment and refresher training

annually.

DAOs: DAOs provide information, data or services that certifying officers rely on to certify

vouchers. Examples include: employees who approve vouchers for payment, travel

authorizing officials, purchase cardholders, and officials who approve time and attendance

records. These officials are responsible for providing timely and accurate data to ensure that

payments are supportable, legal and computed correctly. 31 USC 3528

, Responsibilities

and Relief from Liability of Certifying Officials, reference (d), applies.

Certifying officers and DAOs are to be designated in writing using a DD577 which identifies

the types of payments, roles and responsibilities. Both certifying officers and DAOs are

required to be familiar with their responsibilities as detailed in

31 USC 3528 and DoD FMR

Volume 5 Chapter 5 as they are responsible for providing technical input to financial

management processes and under Public Law 104-106 Section 913, reference (e), they

“shall be pecuniarily liable for any wrong payment or over-obligation of government funds

resulting from his or her negligent performance of duties.” For this reason, accountable

officials must uphold the highest standards with regard to proper payments and obligations of

federal funds.

Fiscal Law and Regulations

SUPSHIP funding must be administered in accordance with laws established by Congress,

as well as policies and regulations promulgated by the Navy and DoD, to enforce the

provisions of proper financial management. The Comptroller is the sub-allocation holder,

and with the Supervisor, is ultimately responsible for establishing tight fiscal controls. The

Comptroller will obtain guidance, as needed, from the NAVSEA Comptroller to resolve any

questions on the interpretation of fiscal laws and regulations.

Purpose, Time and Amount

Purpose, time and amount limit the availability of budgetary resources for obligation and

expenditure. The laws that establish funding control requirements are listed below. There

are three laws that apply to amount violations, which form the cornerstone of the Anti-

Deficiency Act (ADA). Violations of the Purpose and Time statutes may result in an ADA

violation if insufficient funds are available in the correct appropriation to rectify the error.

• PURPOSE (Necessary Expense Doctrine): 31 USC 1301(a)

, Application, reference (f),

states that “appropriations shall be applied only to the objects for which the

appropriations were made except as otherwise provided by law.” There is no

requirement to report a violation of this statute. The accounting, however, must be

corrected to reflect the proper funding. This accounting correction can lead to a

reportable violation of the ADA if the proper funds were not available at the time of the

obligation or expenditure.

• TIME (Bona Fide Needs Rule): 31 USC 1502, Balances Available, reference (g),

states that “the balance of an appropriation or fund limited for obligation to a definite

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

9

period is available only for payment of expenses properly incurred during the period of

availability or to complete contracts properly made within that period of availability and

obligated consistent with section 1501 of this title. However, the appropriation or fund is

not available for expenditure for a period beyond the period unless otherwise authorized

by law.”

• AMOUNT (ADA): 31 USC 1341

, Limitations on Expending and Obligating Amounts,

reference (h), states that “an officer or employee of the United States may not (A) make

or authorize an expenditure or obligation exceeding an amount available in an

appropriation or fund for the expenditure or obligation; (B) involve the Government in any

contract or other obligation for the payment of money before an appropriation is made,

unless authorized by law.”

• AMOUNT (ADA): 31 USC 1342, Limitation on Voluntary Services, reference (i), states

that no officer or employee of the United States will accept voluntary services not

authorized by law, except in cases of emergency involving safety of human life or

protection of property.

• AMOUNT (ADA): 31 USC 1517, Prohibited Obligations and Expenditures, reference (j),

states that an officer or employee of the United States may not make or authorize an

expenditure or obligation exceeding an apportionment or the amount permitted by

regulations prescribed.

Anti-Deficiency Act Violation Reporting

When an obligation or expenditure of funds in excess of the amount available in an

appropriation occurs, the violation must be reported in accordance with the

Financial

Management Regulation (FMR), Volume 14. If a violation occurs at the SUPSHIP level, the

SUPSHIP Comptroller is obligated to notify the Supervisor of the violation within ten working

days and must immediately contact SEA 04Z and SEA 01 with all relevant details. NAVSEA

will conduct a preliminary investigation, to include the advice of legal counsel, to determine if

a violation has occurred and the nature and scope of the violation.

Depending upon the findings and if sufficient funds exist within the appropriation at the

NAVSEA headquarters level, the issue may be resolved in-house. If a violation is confirmed

which cannot be resolved at the Headquarters level, the results of the preliminary review

must be submitted up the chain-of-command to the Assistant Secretary of the Navy

(Financial Management and Comptroller), who will review and forward to the Undersecretary

of Defense (Comptroller), who will perform a final review and determination and, when

necessary, prepare the letters reporting the violation to the President, the Office of

Management and Budget and Congress.

Anti-Deficiency Act Violation Penalties

Penalties for violation of 31 USC 1341 and 1342 are contained in 31 USC 1349, Adverse

Personnel Actions, reference (k), and 31 USC 1350, Criminal Penalty, reference (l), while

penalties for violation of 31 USC 1517 are contained in 31 USC 1518, Adverse Personnel

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

10

Actions, reference (m) and 31 USC 1519, Criminal Penalty, reference (n). In both cases,

violators are subject to appropriate administrative discipline including, when circumstances

warrant, suspension from duty without pay or removal from office. For knowing and willful

violations, the penalty is a fine of not more than $5,000, imprisonment of not more than two

years, or both.

Types of Appropriations

Appropriations

An appropriation is the authority provided by an Act of Congress to incur obligations for

specified purposes and to make payments for them out of the Treasury. The following is a

brief description of the types of appropriations often encountered by SUPSHIPs. They are

generally classified as either expenses or investments. Expenses are the costs incurred to

operate and maintain the organization. Investments are costs that result in the acquisition of,

or an addition to, end items. Refer to the Department of the Navy Financial Policy Manual,

NAVS0 P-1000, reference (o), and DoD FMR Volume 1

for more detailed explanations of

appropriations.

4.4.1.1 Operations & Maintenance, Navy (O&M,N)

O&M,N funds are used for expenses, not otherwise provided for, necessary for the operation

and maintenance of the Navy and Marine Corps, as authorized by law. Per the

Expense/Investment criteria, equipment purchases under this appropriation are limited to a

system unit price of less than $250,000. This limitation is subject to change by Congress,

and the current limitation is contained in the DoD FMR Volume 2A. O&M,N funds are

available for new obligations for one fiscal year and are appropriated and authorized for use

on an annual basis. This appropriation funds SUPSHIPs’ operations and includes salaries,

and general and administrative (G&A) costs. G&A includes the costs necessary to support

the SUPSHIP workforce and typically include costs for IT, travel, and training.

4.4.1.2 Operations & Maintenance, Naval Reserve (O&M,NR)

O&M,NR funds are used for expenses, not otherwise provided for, necessary for the

operation and maintenance, including training, organization, and administration, of the Navy

Reserve; repair of facilities and equipment; hire of passenger motor vehicles; travel and

transportation; care of the dead; recruiting; procurement of services, supplies, and

equipment; and communications. Equipment purchases under this appropriation are limited

to a unit price of less than $250,000. O&M,NR funds are available for new obligations for

one fiscal year and are appropriated and authorized for use on an annual basis.

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

** Link requires CAC/NMCI access

4

-

11

4.4.1.3 Shipbuilding and Conversion, Navy (SCN)

SCN funds are used for investments to finance the construction of new ships and conversion

of existing ships, including service life extensions and nuclear refueling overhauls. Included

in the SCN appropriation are hull, mechanical and electrical equipment, electronics, guns,

torpedo and missile launching systems, and communications systems. It also includes plant

equipment, ship outfitting and post-delivery projects, machines, and tools. This appropriation

is a multi-year appropriation and normally remains available for obligation for five fiscal years

or the obligation work limiting date (OWLD) of the ship under construction. The OWLD is

established as 11 months following completion of fitting out the ship, and the OWLD date of

the last hull in a class of ships governs when the appropriation is scheduled to expire.

NAVSEA 01 has created an SCN Desk Guide**

to assist in the execution of SCN funds.

4.4.1.4 Weapons Procurement, Navy (WPN)

WPN funds are used for investments to finance the procurement of missiles, torpedoes,

guns, munitions, and supporting equipment, and the installation of modernization equipment.

This appropriation is a multi-year appropriation and remains available for new obligations for

three fiscal years.

Other Procurement, Navy (OPN)

OPN funds are used for investments to finance the procurement, production and

modernization of equipment not otherwise provided for. Such equipment ranges from the

latest electronic sensors to training equipment and spare parts. The system unit price of this

equipment must be in excess of $250,000. This appropriation is a multi-year appropriation

and remains available for obligation for three fiscal years.

4.4.1.5 Research, Development, Test and Evaluation (RDT&E)

RDT&E funds are used for expenses and investments for the development of a new system,

such as basic and applied research, advanced technology development, demonstration and

validation, engineering development, developmental and operational testing, and evaluation

of test results. The cost of operation of dedicated research and development installations

and activities are also appropriated under RDT&E. This appropriation is a multi-year

appropriation and remains available for obligation for two fiscal years; however, RDT&E

follows an incremental funding policy and is budgeted to cover the costs expected to be

incurred during a 12-month period.

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

12

4.4.1.6 Navy Working Capital Fund (NWCF)

The Navy Working Capital Fund (NWCF) is a branch of the family of DoD Working Capital

Funds. The NWCF is a revolving fund, an account or fund that relies on sales revenue

rather than direct Congressional appropriations to finance its operations. It is intended to

generate adequate revenue to cover the full costs of its operations, and to finance the fund’s

continuing operations without fiscal year limitations. A revolving fund is intended to operate

on a break-even basis over time; that is, it neither makes a profit nor incurs a loss.

SUPSHIPs are not NWCF activities, but purchase services from, or work with, NWCF

activities.

On occasion, program offices provide funding to NWCF activities for supplies and/or

services. If that funding needs to be placed on a ship building contract, the originating HQ

WBS element needs to be used to create purchase requests rather than using a WCF

reimbursable network activity.

4.4.1.7 Foreign Military Sales (FMS)

FMS trust fund is a transfer from Department of Treasury, through DoD to the Department of

Navy. FMS case funding is a no-year appropriation advance to finance the cost of FMS

purchases. The associated overhead, which is a one-year appropriation is paid for by FMS

Contract Administration Service (CAS) funding.

4.4.1.8 National Defense Sealift Funds (NDSF)

NDSF are used for the construction, operation, maintenance, and support of strategic sealift

assets, such as dry cargo/ammunition ships (T-AKE) and expeditionary platforms like mobile

bases (T-ESB) and fast transports (T-EPF). The NDSF appropriation is a multi-year

appropriation and shall remain available for obligation for five fiscal years.

Budgeting and Accounting

SUPSHIP Mission Budgets

Funding and manpower controls evolve over time and are based on Program Objective

Memorandum (POM) requests as part of the Planning, Programming, Budgeting and

Execution (PPBE) process within DoD. This process for SUPSHIPs begins 30 months in

advance of the beginning of an execution year. The SUPSHIP Workforce Forecasting Tool -

Pricing Model (SWFT-PM) is the model used to project future year manpower and funding

requirements.

Annual Financial Management Plans are developed by SEA 04Z1 for the SUPSHIP

community and provided to SEA 01 for review, consolidation, and integration into NAVSEA’s

submissions to the Department of Navy, Office of the Secretary of Defense and President’s

budget requests. These budgets normally cover the current year and the next fiscal year,

commonly referred to as “the budget years”. Once financial controls for a fiscal year are

known, the division of mission funding to the individual SUPSHIPs is calculated based on

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

13

projected manning requirements (end strength and Full-Time Equivalent (FTE) controls) and

the amount of funding available in the execution year.

During the year of execution, funds are issued by NAVSEA to the SUPSHIPs on a quarterly

basis using fund centers and functional areas within the Navy Enterprise Resource Planning

System (Navy ERP). The allocations are based on obligation phasing plans developed

between the SUPSHIP Comptrollers and SEA04Z1. Adjustments can occur at any time

during the year of execution to accommodate emergent requirements.

SUPSHIPs must review budget requirements quarterly. Requests for adjustments

(increases and decreases) in a quarterly cash allocation or the annual planning amount will

be provided to SEA04Z1 for coordination. In addition, NAVSEA 04Z will conduct a mid-year

review of SUPSHIP mission funding during the January-March timeframe. If a significant

shortfall exists, the SUPSHIP will provide detailed justification to SEA 04Z1 for inclusion in

NAVSEA mid-year review requests.

Navy Enterprise Resource Planning (Navy ERP)

Navy ERP is an integrated financial, acquisition and logistics information technology system

that provides financial and budgetary management for Navy System Commands

(SYSCOMs). It is deployed to the following SYSCOMs and their field activities: Naval Sea

Systems Command (NAVSEA), Naval Air Systems Command (NAVAIR), Naval Supply

Systems Command (NAVSUP), Space and Naval Warfare Systems Command (SPAWAR),

the Strategic Systems Program (SSP), and the Office of Naval Research (ONR). For these

commands, it is the financial system of record. The system interfaces with many external

automated systems to exchange acquisition, financial, payment, manpower and personnel,

and logistics data.

NAVSEA’s transition into Navy ERP began on 1 October 2010. At that point, Navy ERP

became NAVSEA’s system of record for financial transactions using FY11 funds, with the

exception of ship construction or “complex” contracts, which were delayed until 1 April 2011

while the development and testing of ship construction functionality was completed. The

NAVSEA general fund decided not to convert their legacy data into Navy ERP. As a result,

FY10 and prior funding retain the Standard Accounting and Reporting System (STARS) as

the financial system of record, while any transactions using FY11 funding and beyond are

completed in Navy ERP. The only exception would be some FY11 funds that needed to be

obligated on contracts between 1 October 2010 and 1 April 2011, prior to the complex

contracting functionality deploying.

Navy ERP is used by NAVSEA HQ to receive and distribute funding, and by the SUPSHIP to

establish obligations and commitments, create purchase requests and funding documents,

make payments, perform financial reporting, provide financial auditability, and perform

timekeeping. There are workflows within Navy ERP that route documents for approval via

predetermined steps to ensure that funding transactions are appropriately authorized and

valid. Navy ERP also has a document management system that allows attachments to

provide additional information on transactions (such as purchase requests, sales orders, and

project structures) and for auditability. As an integrated system, financial managers, project

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

14

offices, and contracting officers all have access to the areas they need to perform work

within the system, and although each group has different responsibilities, they are looking at

the same data to accomplish it.

4.5.2.1 Roles in ERP

Navy ERP relies on specific role assignments for access. Roles are requested via a system

called Access Enforcer. Role based training is required prior to obtaining a role, and roles

are monitored closely by the individual commands and the NAVSEA ERP Business Office

(NEBO) to ensure access to information and transactions are provided on an as-needed

basis. In addition, some role combinations are restricted and/or require specific justification

as a part of management and controls that help ensure the accountability of financial data

and prevent waste, fraud, and abuse. OMB Circular A-123

, Management’s Responsibility for

Enterprise Risk Management and Internal Controls, reference (p), states that internal

controls are an integral part of all financial management processes and requires that

reasonable assurance be taken to ensure effective operations, reliable financial reporting,

and compliance with applicable laws and regulations. Further control activities stated in

Standards of Internal Control in the Federal Government (“Green Book”),

GAO-14-704G,

reference (q), prescribe proper segregation of duties (separate personnel with authority to

authorize a transaction, process the transaction, and review the transaction); physical

controls over assets (limited access to inventories or equipment); proper authorization; and

appropriate documentation and access to that documentation. As a result of this guidance, a

separation of duties (SOD) analysis is required to be completed annually by all NAVSEA field

activities for individuals that possess conflicting role combinations, and justification

documentation is required for all SOD role combinations that will be maintained.

4.5.2.2 ERP Site Leads

Navy ERP touches everyone and many processes at the SUPSHIPs. It is important to be

aware of methods to troubleshoot any issues that might arise. Each NAVSEA command,

including the SUPSHIPs, has a site lead for ERP. These site leads can assist in getting the

information necessary to obtain roles or assist in solving other Navy ERP issues that may

arise. The first step and fastest way to resolve an issue is to leverage subject matter experts

within the command or within the SUPSHIP community. If that fails, there is a HEAT ticket

system on the Navy ERP website for registered issues. These HEAT tickets will initially go

to the Navy ERP help desk at NAVAIR, and if they cannot be resolved at that level, may be

forwarded to NEBO for resolution. If the NEBO is unable to resolve the issue, it may

continue to the Navy’s ERP Program Office at NAVSUP for resolution.

The Standard Accounting and Reporting Systems (STARS)

STARS was the official accounting system for NAVSEA and most Navy organizations until

the implementation of Navy ERP. Most Navy System Commands have now transitioned to

Navy ERP although Fleet units are still using STARS. NAVSEA financial data resides in

STARS for all FY10 and prior years. The SUPSHIPs have access and use both the STARS-

HCM and the STARS-FL modules to maintain legacy accounting and general ledger data. A

description of the current STARS sites is below:

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

15

STARS-FL Charleston – Official accounting system for SUPSHIP Mission Funding and

Reimbursable Funds Administration through FY10. SUPSHIPs continue to use this site to

reconcile FY10 and prior year accounts.

STARS-FL Norfolk – Official accounting system for Fleet funded ship work actions.

SUPSHIPs use this site to reconcile accounts prior to FY11. Since implementing ERP in

FY11 SUPSHIPs only use STARS-FL Norfolk to assist in the reconciliation of direct cited

actions.

STARS-HCM – Official accounting system for the Navy’s System Commands and PEOs

prior to ERP. These commands implemented ERP at different times and vary as to the

conversion of legacy data. Ship work funded in STARS HCM that was not converted to ERP

will continue to be reconciled from STARS. For NAVSEA General Fund, legacy data was not

converted, and STARS HCM remains the accounting system for all funds FY10 and prior.

These funds are referred to as “legacy funds”. Some FY11 funds are maintained in STARS-

HCM because they were obligated in FY11 prior to the April 1, 2011 Complex Contract

implementation in Navy ERP.

Purpose of Funds Provided to SUPSHIPs

SUPSHIP Mission Funds

The SUPSHIPs are mission-funded activities financed with appropriated O&M,N funds.

Department of the Navy Financial Policy Manual, NAVSO P-1000

, provides guidance in

budget execution and financial management of funds used to finance the salaries and

general and administration expenses (G&A) incurred in the daily operation of the SUPSHIPs.

Ship Construction Funds

The Program Executive Offices (PEOs) budget for and fund ship new construction programs

and carrier refueling overhauls (RCOH) from SCN and RDT&E appropriations. Based on

program managers’ estimates, NAVSEA prepares annual budget requests which are

submitted for review. The budget process follows the same process as SUPSHIP O&M,N,

and calls for sequential submissions up the chain starting with the Navy Budget in the

summer, the Office of the Secretary of Defense (OSD) Budget normally submitted in the fall,

and culminates in the President’s Budget submission to the Office of Management and

Budget (OMB) in February of each year. Once the funding is made available to the program

offices in the year of execution, funding for various items is made available to the SUPSHIPs

in Navy ERP via a Work Breakdown Structure Element (WBSE) as part of a Budget

Structure. The program office creates a Budget Structure that projects their program

spending plan for that year/appropriation. Each WBS reflects a category of cost for the

program. The WBSE is communicated to the SUPSHIP typically through an email and gives

the SUPSHIPs direction on execution (purpose and amount).

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

16

Foreign Military Sales (FMS) Funds

Foreign Military Sales (FMS) provide military assistance through the sale of defense articles

and services to eligible foreign governments and international organizations. Each FMS

project is assigned a case order number for accounting and management purposes. The

United States normally receives full reimbursement for costs associated with these sales.

Most sales are made on a "dependable undertaking" basis. To ensure that the U.S.

Government will not suffer a loss resulting from the sale, the foreign government agrees to

provide cash to cover payments to contractors and to reimburse the Department of the Navy

for work performed. Initially, most obligational authority is in the form of unfunded contract

authority where the cash needed for expenditures is not available. Defense Finance and

Accounting Service (DFAS) is responsible for obtaining the required cash, as needed, from

foreign customers on a quarterly basis. DFAS applies for FMS Authority when an invoice

has FMS lines of accounting. All other lines on the invoice must be pre-validated before

DFAS will apply for the FMS authority. FMS authority is only granted after the first Friday of

the month and not after the third week of the month. Monetary rates come out at the

beginning of the month and DFAS wants to ensure that the current rate is used, hence not

applying until the first Friday. DFAS will not apply after the third week of the month because

they have to ensure that the invoice pays during that month and is paid at the previous rates.

Funding for labor, material, contracts, travel, accessorial, and all other costs of work directly

identifiable to an FMS case is sent from NAVSEA 01 to SUPSHIP via an ERP Direct Cite

(RX) document in ERP. Management Information System for International Logistics (MISIL)

is the financial system of record for FMS. Obligations are created in the ERP system, and

also posted in MISIL. Disbursements are merged from Wide Area Workflow (WAWF) to

MISIL. Funding for FMS Contract Administration Services (CAS) is provided to SUPSHIP

from NAVSEA 01 via an ERP reimbursable (WX) funding document. CAS charges are

expenses not directly identifiable to an FMS case, and consist of administrative overhead

labor and other costs that support all FMS projects. DoD FMR Volume 15

provides

additional information regarding financial management of FMS.

Ship Repair Funds

The Fleet Commands (FLTCOMs) budget and fund ship repairs from O&M,N and O&M,NR

appropriations, as applicable. The funds are normally authorized to SUPSHIP for specific

use by the Type Commander (TYCOM) responsible for a ship. These funds pay for

contractual costs of authorized repairs and for incidental costs, which include:

• Naval Supervising Activity (NSA) material

• Travel and salary cost for overseas ship checks

• Alterations Equivalent to a Repair (AERs) and preparation of drawings or sketches to

be contracted out

• Electronics field changes on installed equipment

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

17

SUPSHIPs receive ship repair funds from FLTCOMs on NAVCOMPT Form 2276, commonly

referred to as a Request for Contractual Procurement (RCP), and NAVCOMPT FORM 2275

Order for Work and Services. Details on ship repair funds, including current year and prior

year availabilities, may be found in the Department of the Navy Financial Management Policy

Manual,

NAVSO P-1000, paragraphs 074200 and 074220.

Fleet Modernization Program (FMP) Funds

Installation of equipment is funded with the OPN appropriation in the same fiscal year as

funds that procure the associated equipment. NAVSEA provides funds to SUPSHIPs on

WBS elements for the accomplishment of Title “K” Ship Alterations (SHIPALTs), electronics

field changes for installed equipment, and ordnance alterations (ORDALTs). This funding

covers expenses incidental to the accomplishment of alterations, such as:

• Preparation and reproduction of alteration drawings contracted out

• Travel costs, other than local, for overseas shipchecks of alterations

Title “D” and “F” SHIPALTS are addressed in paragraph 4.7.2.

Berthing Funds

Berthing is a very complex issue due to the various types of funds that are used to pay these

expenses. 10 USC 7572

, Quarters: Accommodations in Place of for Members on Sea Duty,

reference (r), provides for accommodation of members on sea duty or assigned to duty in

connection with commissioning or fitting out of a ship deprived of quarters, onboard a ship

because of repairs, because the ship is under construction and is not yet habitable, or

because of other conditions that make quarters uninhabitable. Expenses can be funded by

SCN, TDY or military allowances, depending on the type of orders issued to the sailor. For

SCN funded ship availabilities, the cost of berthing is part of the investment cost of the

availability and may be funded by NAVSEA using SCN or O&M,N funds, depending on the

Program Office’s election of funds at the beginning of the availability and must remain in the

chosen appropriation for the life of the availability. For O&M,N funded ship availabilities, the

cost of berthing is funded by the FLTCOM in the O&M,N appropriation. Berthing for

crewmembers of new construction platforms varies based on several factors.

For surface ships, crew members are ordered to ships under construction as either a

member of the Pre-Commissioning Unit (PCU) that is geographically located at the

shipbuilder’s yard, or as part of the Pre-Commissioning Detachment (PCD) which is located

at a fleet concentration area, normally in the projected homeport of the ship being built. For

nuclear-powered ships, crew members are ordered directly to the PCU at the shipbuilder’s

yard. PCU members are ordered to the ship in increments. Some of these increments are

for a period of time greater than 180 days before delivery. In these circumstances, the

member is issued orders “For Duty In Connection With Fitting Out (DUTY CFO) (ACC-106)”,

which allows the member to execute a Permanent Change of Station (PCS). The member is

entitled to:

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

18

• Move family members/household goods to the PCU

• Receive basic allowance for housing (BAH) or government quarters, if available

A second set of PCS orders will be issued entitling the member to move family members and

household goods to the ship's ultimate homeport once it has been designated.

If the crew member will be at the PCU less than 180 days, the orders are written as

Temporary Duty In Connection With Fitting Out (TEMDU CFO/ACC-352), with the ultimate

duty station designated as the ship in its selected homeport. These orders do not authorize

PCS to the shipbuilder’s yard. The member is entitled to per diem while on TEMDU at the

PCU, and to move family members/household goods to the post-commissioning homeport

after the Chief of Naval Operations (CNO) makes the official homeport announcement. Per

diem ceases at the scheduled date of delivery for surface ships and at the designated move

aboard date for carriers and submarines. Carrier and submarine move aboard dates are

generally earlier than the delivery date. At delivery the ship should be habitable. If the Navy

accepts delivery of a ship that is uninhabitable, program managers are responsible to pay for

pre-com crew housing using SCN end cost or O&M,N funds until the ship becomes

habitable.

The administrative division of the PCU processes military orders for assigned crewmembers

and verifies who is entitled to government quarters. The PCU is also responsible for

providing that information to the installation responsible for arranging military or commercial

berthing. If SCN funded berthing is required, the SUPSHIP Comptroller receives funding

from the program office in order to pay the cost of the required berthing. Certification of

entitlement from the PCU is used to validate the payment. After commissioning, berthing

expenses become the responsibility of the Fleet.

The feeding or messing of the pre-com crews is not an allowable cost. Military members

receive a Basic Allowance for Subsistence (BAS) which is a cash allowance to offset the cost

of a member’s meals.

Commander Naval Installations (CNI) Funds

Commander Naval Installations Command (CNIC) has overall shore installation

management responsibility and authority as the Budget Submitting Office (BSO) for

installations support and is the Navy point of contact for installation policy and program

execution oversight. Base support responsibilities vary by region and SUPSHIP. In some

cases, funding is transferred to the SUPSHIPs for purchase of cell phones, long distance

service, and vehicles.

Environmental Compliance Oversight Funds

Environmental Compliance Oversight funds are used to support the SUPSHIPs’

Environmental, Safety and Health (ESH) programs. This funding supports salaries of civilian

personnel involved in ESH programs, projects to ensure that contractor oversight in the ESH

arena is effectively conducted, and awareness training that is provided to the contractor,

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

19

SUPSHIP and ship’s force personnel. Environmental funding is coordinated between

NAVSEA 04Z and 04RE and provided to the SUPSHIPs as part of mission funding.

Reimbursable Work Orders (RWO)

In addition to the funding provided for contractual obligations, SUPSHIP customers provide

reimbursable funding to pay for non-mission work accomplished by the SUPSHIPs.

Examples include out-of-build yard post shakedown availabilities (PSAs), Deputy Program

Manager’s Representatives and production controllers. This funding is provided annually,

and is documented via the RWO process. To determine whether work is considered mission

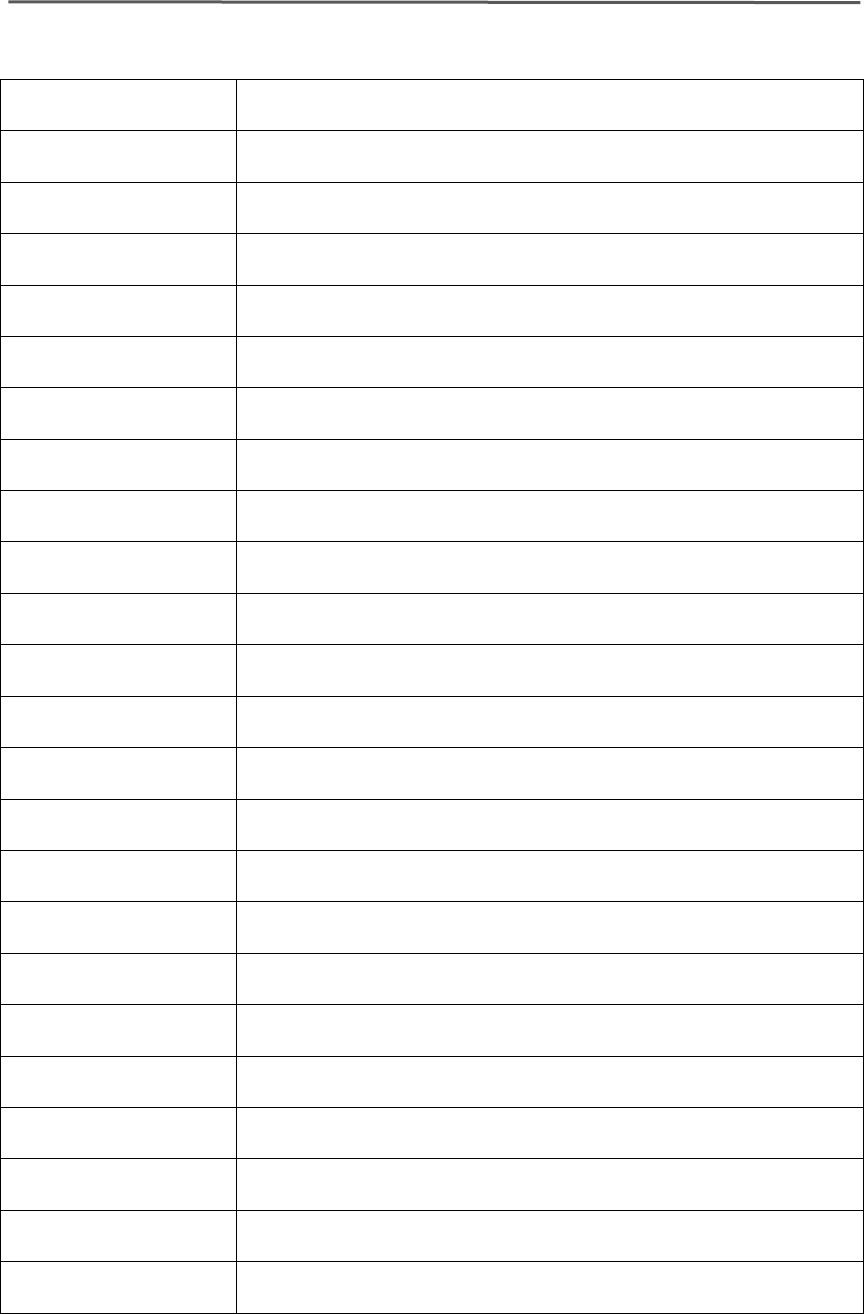

or non-mission, see the SUPSHIP Funding Decision Tree, Figure 4-1

.

Funding Methods

Mission Funding Allotment

An allotment is a distribution of budget authority to an execution level accounting entity. It

authorizes the incurrence of obligations in a specified amount for the purpose of the

SUPSHIP mission as described in the budget submission. NAVSEA provides O&M,N

funding to each SUPSHIP’s highest level fund center within Navy ERP. The SUPSHIP

Comptroller monitors and controls the allocation to lower levels within the command using

statistical project structures. All funding is required to be administered in accordance with

existing laws and statutes, some of which are described in paragraph 4.3

of this chapter.

Reimbursable Orders

Reimbursable orders are written agreements between components of the Federal

Government requiring the performance of work or services by one component and payment

by the other component which cover the cost of property, work or services. The DoD FMR

Volume 3, Chapter 15 provides general reimbursement policy. DoD FMR Volume 11A

contains more detailed guidance regarding reimbursable operations, policies and

procedures. All funded, reimbursable orders, including those of an Economy Act Order

(EAO) per Assistant Secretary of the Navy (Financial Management and Comptroller)

(

ASN(FM&C)) memo dated 3 May 2002, reference (s), are subject to the recipient activity

projecting that at least 51 percent of the funds will be used for "in-house" work. “In-house”

work is defined as the cost of all direct labor, materials and supplies, travel and minor

equipment. If less than 51 percent of the work will be in-house effort, the funding for tasks to

be contracted out should be provided on a Request for Contractual Procurement (RCP).

SUPSHIPs should not accept reimbursable orders when no in-house salaries are to be

charged, with the exception of reimbursable documents for the sole purpose of executing

MILSTRIP requisitions. MILSTRIP requisitions are a specific exception to the 51% rule

granted due to limitations in the ERP system. Reimbursable order accounting requires

additional SUPSHIP effort in order to support documentation and accounting workload.

Policy

In accordance with FMR Volume 11A, an activity performing a service or furnishing material

to another entity shall be reimbursed unless the performing entity has been provided

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

20

appropriated funds for that purpose. Because SUPSHIPs are provided appropriated funds

for the purpose of performing their assigned mission, they may only accept reimbursable

orders for work that falls outside the scope of their mission. Failure to comply with this

requirement could result in a violation of 31 USC 1301 (Purpose Act), and possibly

31 USC

1341 (ADA) as well.

The SUPSHIP Funding Decision Tree, Figure 4-1, was developed to assist SUPSHIPs in

determining whether a customer requested task falls within or outside the scope of the

SUPSHIP mission. The decision tree asks a series of general questions that apply to all

tasks, and if necessary, follows with additional questions based on the nature of the tasking

and the mission area under which the tasking would fall. SUPSHIP personnel should

request SEA 04Z1 assistance in resolving any tasking that is not clearly addressed by the

Decision Tree.

4.7.2.1 Types of Reimbursable Orders

Project Order (PO)

A project order is a specific, definite and certain order issued under the authority contained in

41 USC 23

, Orders or Contracts for Material Placed with Government-owned Establishments

Deemed Obligations, reference (t), for the production of material; for repair, maintenance, or

overhaul; or for other specific work and services to be performed. It serves to specifically

define the work to be accomplished and the terms of the order in much the same manner as

contracts with a commercial enterprise. Project orders, once issued, can carry over until

completion. However, similar to contracts, project orders must be for hardware or a 'non-

severable' service only.

Funds shall be obligated when the performing activity signs acceptance of the project order.

The accounting is the responsibility of the accepting activity. The funds provided on a project

order cannot be exceeded without written amendment by the ordering activity and are

subject to the same fiscal limitations that are contained within the appropriation from which

they are funded. Expiration dates of project orders may not extend beyond the point in time

in which the ordering appropriation will be cancelled (generally, five years after the

appropriation expires for new obligations). Because of the expiring funds limitation, the order

must stand the test of a bona fide need to be issued in the current fiscal year and a bona fide

intent that the performing activity intends to proceed with the execution of the request without

undue delay.

Project orders are subject to the recipient activity projecting that at least 51 percent of the

funds will be used for "in-house" work. If less than 51 percent of the work will be in-house

effort, the funding for tasks to be contracted out should be provided on an RCP, Request for

Contractual Procurement. When funding is sent via a Project Order to another Navy activity,

for legacy funds, the NAVCOMPT Form 2275 is used, however in ERP the

NAVCOMPT

Form 2276A is generated.

Economy Act Order (EAO)

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

21

Like the project order, an Economy Act Order provides authority for federal agencies to order

goods and services from other federal agencies, including other military departments and

defense agencies. The order is issued, however, under the authority contained in 31 USC

1535, Agency Agreements, reference (u), and is intended for work or services of a recurring

nature where the scope of the work is not specific. These orders are typically used for inter-

service support agreements for services such as administrative or janitorial work, utilities,

and transportation. However, services such as testing and evaluation and level of effort

work-years may be covered by an EAO. Funding for EAOs for legacy funds is sent using the

NAVCOMPT Form 2275, however in ERP a NAVCOMPT Form 2276A is generated. This

form is commonly called a “work request.” EAOs are subject to the recipient activity

projecting that at least 51 percent of the funds will be used for "in-house" work. If less than

51 percent of the work will be in-house effort, the funding for tasks to be contracted out

should be provided on an RCP, Request for Contractual Procurement. MILSTRIP

requisitions, funded reimbursably from funding sources external to ERP, are a specific

exception granted due to limitations in the ERP system.

Funds for EAOs are obligated upon documented acceptance by the performing activity. The

accounting for these funds becomes the responsibility of the performing activity. The funds

provided by an EAO cannot be exceeded without written amendment by the ordering activity.

An EAO citing an annual or multi-year appropriation must serve a bona fide need arising or

existing in the fiscal year (or years) for which the appropriation is available for obligation.

Work requests must terminate upon expiration of the appropriation cited on the document.

Military Interdepartmental Purchase Request (MIPR)

MIPRs provide authority to order material, supplies, equipment, work, and services between

Department of Defense activities and federal agencies. MIPRs can be received or issued by

SUPSHIPs for orders placed with non-Navy DoD activities and federal agencies via

DD Form

448. For MIPRs issued by the SUPSHIPs, obligations will be recorded upon contract award

for direct cite MIPRs, and upon acceptance for reimbursable orders. Examples of MIPR use

include: orders placed with the GSA, Federal Prison Industries, Government Printing

Offices, Defense Supply Agencies, printing plants authorized to be established by the Joint

Committee on Printing, and the Navy Publications and Printing Service Management Office.

Many orders placed with these agencies are required by law.

Direct Citations

Direct citations are requests from one government activity to another to obtain material,

equipment or services. The requesting activity provides their accounting data and the

performing activity cites the requesting activity's complete line of accounting directly on the

document. If both activities are in ERP, the line of accounting is conveyed using Budget

Structure WBS elements or Network Activities. For Navy Activities outside of Navy ERP,

requests for Contractual Procurement (RCP) can be issued on either the

NAVCOMPT Form

2276 or 2276A to pass direct citation authority. The accounting function remains the

responsibility of the requesting activity and its AAA. When the performing activity signs

acceptance, they are agreeing to award the contract; however, direct cite obligations are not

recorded until the contract is awarded. The performing activity must comply with fiscal law

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

22

and all restrictive statements contained in the document and ensure that confirmed copies of

the contracts or orders that result are promptly provided to the requesting activity and its

AAA for posting of obligations and expenditures. The reimbursable portion of a NAVCOMPT

2276A will be obligated upon acceptance. The funding cited on the document will not be

exceeded without an amendment issued by the requesting activity.

Budget Structure WBS Elements from ERP Activities

Once a program has created their Budget Structures and associated WBS elements, they

can use those WBS elements to pass funds to other activities for various execution

purposes. For activities within Navy ERP, the Budget Structure WBS element acts for the

line of accounting and is provided for direct citation on contract award, as well as other

funding transactions like outfitting, pre-commissioning, MILSTRIPs, P-Card, etc.

General Classifications of Funds Transactions

All expenditures must be preceded by an authorization to expend from the available funds.

In theory, every transaction progresses through four stages: initiation, commitment,

obligation, and expenditure. The four stages of funds transactions are described as follows:

• Initiation: An administrative reservation of funds based on procurement directives,

requests, or equivalent instruments that authorize preliminary negotiations, but require

that funds be certified by the official responsible for the administrative control of funds

before incurrence of the obligation. Initiations are entered into memorandum accounts to

help keep pre-commitment actions, such as approved procurement programs, within the

available subdivision of funds. Initiations identify funds to be set aside for planning

purposes before establishment of commitments or obligations. Initiations will not be

maintained as a part of the official fiscal records. At the field level, this is done on an

exception basis, for example in planning yard contracts.

• Commitment: An administrative reservation of funds based on firm procurement

requests, unaccepted customer orders, directives, authorizations to issue travel orders,

or equivalent instruments which authorize the recipient to create obligations without

further recourse to the official responsible for certifying the availability of funds. A

commitment is generally recorded when the Comptroller signs the document to certify

that the funds are available and properly cited for the effort. Only warranted or

authorized personnel can legally obligate government funds. In ERP, a commitment is

recorded when a PR is created and saved. It is then sent through workflow to the

Comptroller for approval before a legal obligation can occur.

• Obligation: A legally binding agreement or action that will result in outlays, immediately

or in the future. An obligation is a recording of funds when an order is placed, contract is

awarded, service is received, travel orders are issued, and similar transactions are

entered into requiring future payment of money in an agreed amount. By law, obligations

must be supported by documentary evidence of a mutual agreement in writing. Each

individual transaction must meet the test of the following principles:

S0300-B2-MAN-010 Rev 2, Change #27 Chapter 4, Revised 18 August 2019

SUPSHIP Operations Manual (SOM) Reference/hyperlink updates

4

-

23

o A determination that the specific goods, supplies or services required according

to a contract entered into or an order placed obligating an appropriation to meet a

bona fide need of the fiscal year charged; and

o Contracts entered into or orders placed for goods, supplies or services will be

executed only with a bona fide intent that the performing activity will commence

work and perform the contract without unnecessary delay.

• Expenditure: An accounts payable transaction and its corresponding disbursement that

results in a reflection of expenditures. The Debt Collection Improvement Act of 1996,

Public Law 104-134

, reference (v), requires payments on all federal contracts to be made

via Electronic Funds Transfer (EFT) if the solicitation was issued after June 26, 1996.

DoD FMR Volume 5 Chapter 11 applies. All DoD Vendors are required to be registered

in the System for Award Management (SAM) database as DFAS payment offices and the

SUPSHIPs use the EFT data provided in the SAM in order to issue EFT payments.

There are only limited exceptions to this mandate.

Prompt Payment Act, 5 CFR 1315

In 1982, Congress enacted the Prompt Payment Act, PL 97-177 (now 5 CFR 1315),

reference (w). The Prompt Payment Act was passed to help ensure federal agencies pay

vendors in a timely manner, pay interest when payments are made late, and take discounts

only when payments are made by the discount date. The Prompt Payment Act requires an

assessment of late interest penalties against agencies that pay vendors after a payment due

date. The late payment interest rate was established under the Contract Disputes Act and is

referred to as the "Renegotiation Board Interest Rate," the "Contract Disputes Act Interest

Rate," and the "Prompt Payment Act Interest Rate."

Progress Payments and Prompt Payment Requirements

Per DoD FMR Volume 10 chapter 7, progress payments and interim vouchers on cost

contracts are not subject to the Prompt Payment Act. They are considered to be contract

financing payments and are paid based on specific payment terms contained in the contract.

Department of Defense policy is to make contract financing payments as expeditiously as

possible. The standard due date unless otherwise specified is 7 days for progress payments

on fixed price contracts and 14 days for interim vouchers on cost contracts.

S0300-B2-MAN-010 Rev 2, Change #24 Chapter 4, Revised 17 August 2018

SUPSHIP Operations Manual (SOM) Minor format and hyperlink corrections

4-

24

Figure 4-1: SUPSHIP Funding Decision Tree

Adminis trative

Clerical, legal, personnel

admin, training, ESH, IT

support, etc.

Contracting/Financial

ACO, PCO, MSR/ABR

support, cost accounting,

etc.

Ma ter ia l/ILS

Matl/equipment mgmt,

inventory control, shipping,

receiving, etc.

Technical

Eng, design, waivers/dev, QA,

config. control, testing,

certification, trials, etc.

Sta rt

Project Mgmt/Coord.

Waterfront management &

coordination of a project in

execution/production.

Is task primarily associated

with admin support to the

command (SUPSHIP)?

Is task requested by a

DoD customer?

For repair/modernization/

RCOH work, is task in support

of contract/contractor under

command’s cogni zan ce p er

DCMA CAS Directory?

Gener al

No

Yes

Yes

Yes

Yes

Reimb.

Funding

Reimb.

Funding

Mission

Funding

Mission

Funding

Mission

Funding

Is task related to management

of o ff -ship berthing and

messing facilities for ships

for ce?

Is task related to training or

certification of ships force?

Mission

Funding

Does task involve functions

transferred to NAVSUP? (see

NFLC MOA)

Does task involve managing/resolving

tech issues not associated with an

assigned or anticipated contract?

Is task part of preliminary design/build

team processes or IPTs that influence

contract desi gn or d etail d esig n a nd ar e

not an en gineeri ng sur veil lan ce ta sk

per FAR 42.302(40)?

Is task primarily related to

managing material,

equipment, or equipment

maintenance for ships force

work?

Is task primarily associated with

oversight, testing, crew trng/cert, or

trials for major ship systems procured

through a contract not under SUPSHIP

cognizance?

Is task primarily related to maintaining

configuration control of class standard

components?

Is task primarily involved with

managing class-wide or programmatic

issues wi th oth er SUPSH IPs, or with

shipbuilders not under command’s

cognizance?

Is task related to lo ng -term, life cycle

initiatives on one or more in-service

ships?

Pass to

NAVSUP

Reimb.

Funding

Yes

Yes

Yes

No

No

No

No

Yes

Yes

Yes

No

No

No

No

No

Yes

No

Yes

No

No

No

NOTE: If necessary, solicit

RMC support for tasks in

suppor t of repair /moderni zatio n

work that would normally be

performed by local RMC.

Mission

Funding

Yes

No

Yes

Is task related to a cu stom er

teaming or improvement initiative

that requires departure from

SOM gu ida n ce?

Yes

No

No

(see note

below)

Is contract for ship design,

ship construction or repair?

NOTE: If task is a CAS

function but SUPSHIP is not

designated CAS activity,

refer to the appropriate

MOAs between DC MA and

SUPSHIPs.

Is work being performed by

a contr actor assigned i n

CAS-D to a SUPSHIP in

the listed geographic area?

No

Is task non-O&M N fun de d a nd is

the work accomplished by a

production controller or the

deputy PMR in direct support of

the pr ogram?

Is the SUPSHIP the PCO or

assigned as the AC O?

Yes

No

NOTE: N FLC Annex

employees are responsible

for providing their own

equipment but are allowed to

hook up to network due to

collo catio n, so su pp or t is

provided as part of mission

but they provide own equip.

General Function Specific

Yes

Reimb.

Funding

Yes

Is task primarily in support of an

Advance Procurement contract for

which the SUPSHIP is not ACO?

Yes

No

S0300-B2-MAN-010 Rev 2, Change #24 Chapter 4, Revised 17 August 2018

SUPSHIP Operations Manual (SOM) Minor format and hyperlink corrections

** Denotes secure hyperlink requiring NMCI/CAC access

4-25

Chapter 4 Acronyms

AAA Authorized Accounting Activity

ADA Anti-Deficiency Act

AER Alteration Equivalent to a Repair

ASN(FM&C)

Assistant Secretary of the Navy (Financial Management and

Comptroller

BAH Basic Allowance for Housing

CAS Contract Administration Service

CFR Code of Federal Regulations

CNI Commander, Naval Installations

CNIC Commander, Naval Installations Command

CNO Chief of Naval Operations

DAO Departmental Accountable Official

DFAS Defense Finance and Accounting Service

DoD Department of Defense

DoN Department of the Navy

EAO Economy Act Order

EFT Electronic Funds Transfer

ERP Enterprise Resource Planning

ESH Environmental, Safety and Health

FLTCOMs Fleet Commands

FMP Fleet Modernization Program

FMS Foreign Military Sales

FMR Financial Management Regulation

S0300-B2-MAN-010 Rev 2, Change #24 Chapter 4, Revised 17 August 2018

SUPSHIP Operations Manual (SOM) Minor format and hyperlink corrections

** Denotes secure hyperlink requiring NMCI/CAC access

4-26

FTE Full Time Equivalent

G&A General and Administrative

GSA General Services Administration

HQ Headquarters

IT Information Technology

LOA Letter of Authority

MICP Managers’ Internal Control Program

MILSTRIP Military Standard Requisitioning and Issue Procedures

MIPR Military Interdepartmental Purchase Request

MISIL Management Information System for International Logistics

NAVAIR Naval Air Systems Command

NAVCOMPT Navy Comptroller

NAVSEA Naval Sea Systems Command

NAVSEASYSCOM Naval Sea Systems Command

NAVSO-P Navy Financial Policy Manual

NAVSUP Naval Supply Systems Command

NDSF National Defense Sealift Funds

NEBO NAVSEA ERP Business Office

NFLC NAVSUP Fleet Logistics Center

NSA Naval Supervising Activity

NWCF Navy Working Capital Fund

O&M,N Operations and Maintenance, Navy

O&M,NR Operations and Maintenance, Navy Reserve

OMB Office of Management and Budget

S0300-B2-MAN-010 Rev 2, Change #24 Chapter 4, Revised 17 August 2018

SUPSHIP Operations Manual (SOM) Minor format and hyperlink corrections

** Denotes secure hyperlink requiring NMCI/CAC access

4-27

ONR Office of Naval Research

OPN Other Procurement, Navy

ORDALT Ordnance Alteration

OSD Office of the Secretary of Defense

P-Card Purchase Card

PCD Pre-Commissioning Detachment

PCS Permanent Change of Station

PCU Pre-Commissioning Unit

PEO Program Executive Office

PL Public Law

POM/PR Program Objective Memorandum/Program Review

PPBE Planning, Programming, Budgeting and Execution

PSA Post Shakedown Availability

RCOH Refueling Complex Overhaul

RCP Request for Contractual Procurement

RDT&E Research, Development, Test and Evaluation

RWO Reimbursable Work Order

SAM System for Award Management

SCN Ship Construction, Navy

SECNAVINST Secretary of the Navy Instruction

SHIPALT Ship Alteration

SOM SUPSHIP Operations Manual

SPAWAR Space and Naval Warfare Systems Command

SSP Strategic Systems Program

S0300-B2-MAN-010 Rev 2, Change #24 Chapter 4, Revised 17 August 2018

SUPSHIP Operations Manual (SOM) Minor format and hyperlink corrections

** Denotes secure hyperlink requiring NMCI/CAC access

4-28

STARS Standard Accounting and Reporting System

STARS-FL Standard Accounting and Reporting System Field Level

STARS-HCM

Standard Accounting and Reporting System Headquarters

Claimant Module

SUPSHIP Supervisor of Shipbuilding, Conversion and Repair, USN

SWFT-PM SUPSHIP Workforce Forecasting Tool/Pricing Model

SYSCOMs Systems Commands

TDY Temporary Duty

TEMDU CFO Temporary Duty in connection with Fitting Out

TYCOM Type Commander

USC United States Code

WBSE Work Breakdown Structure Element

WBS Work Breakdown Structure

WCF Working Capital Fund

WPN Weapons Procurement, Navy